Mike Tribble of Yeo & Yeo Inducted into National Association of Home Builders’ Society of Honored Associates

Yeo & Yeo CPAs & Business Consultants, a leading Michigan accounting firm, is pleased to announce that Michael T. Tribble, CPA, received the National Association of Home Builders’ (NAHB) Society of Honored Associates award.

“Mike’s tireless commitment to the NAHB is greatly appreciated by many staff and volunteer leaders. He has been an influential and effective participant in a number of budget, financial and audit matters,” says Eileen Ramage, CPA, CAE, Chief Financial Officer of NAHB.

Tribble was inducted in January at the NAHB International Builders Show in Orlando, Florida. He was nominated by both the Home Builders Association of Saginaw and the Home Builders Association of Michigan. The award is given annually to four associate members nationally. Tribble received the award for his years of dedication – most recently he devoted innumerable hours to working with NAHB staff in the development of an updated system of cost allocation, and provided guidance with the association’s 2017 budget. Tribble also worked with NAHB staff to produce a video for NAHB members featuring the Internal Revenue Service Form 990 nonprofit tax return, highlighting the parts of the form that are most important for NAHB members.

Tribble has been committed to the construction industry throughout his career at Yeo & Yeo. He serves on the NAHB board of directors and is chair of its audit committee. He also serves the Michigan Association of Home Builders as a director, chair of its investment and audit committees, and past chair of its Associates Council. He is past president of the Home Builders Association of Saginaw and a member of the Construction Industry CPAs/Consultants Association.

Tribble is a Principal in Yeo & Yeo’s Saginaw office and a member of the firm’s Tax Services and Construction Services Groups.

Operating reserves are not a luxury—they are a necessity for financially savvy nonprofits. Organizations without adequate operating reserves leave themselves vulnerable to the financial instability and damaged reputation that interruptions in incoming revenue might bring.

A recent report from the Nonprofit Finance Fund, a community development financial institution, indicates that operating without an adequate financial cushion is fairly widespread among nonprofits. The Fund’s 2015 State of the Nonprofit Sector Survey results showed that 53% of nonprofits responding had less than three months’ cash on hand and 12% had less than 30 days’ cash in reserve.

What reserves are—and are not

Operating reserves can be defined as the portion of unrestricted net assets that nonprofits designate for use in emergencies or to sustain financial operations in the unanticipated event of significant unbudgeted increases in operating expenses or losses in operating revenues. Reserves should be liquid or easily converted to cash, so the organization is not forced to sell long-term investments, take out a loan or pursue other undesirable alternatives to quickly generate funds.

Also remember that cash on hand is not the same thing as operating reserves. Cash can be restricted for specific purposes while operating reserves must be available to be spent on current operations.

Operating reserves also should not be confused with donor-restricted endowments. Only the income from these endowments is available to be spent (based on the donor’s wishes), with the principal portion held in perpetuity and, thus, unavailable for daily operations.

Why you need reserves

Remember the last recession? The years following the financial crisis of 2008 were challenging for many nonprofits, with plummeting revenues that led to painful cuts in staffing and programs—despite, at times, an increased demand for services. Some nonprofits shut down altogether. When a turbulent economy reduces revenues to a trickle, operating reserves can help organizations survive.

Healthy reserves also will allow your organization to seize opportunities that require a cash outlay (for example, purchasing a building), set aside funds for long-term goals and plans, and cover unexpected expenses after a natural disaster or other emergency. Reserves also can prove valuable when you need to augment your staff and deliver services under federal contracts that will not provide payment for 30 to 60 days.

How much to set aside as reserves

The Nonprofit Operating Reserves Initiative Workgroup, an all-volunteer group of nonprofit leaders, financial management consultants and others, suggests nonprofits consider several issues when setting a dollar goal for their reserves:

- Are your revenue sources subject to large, unexpected, negative fluctuations?

- Are your resources subject to sudden increases in demand?

- Are your income and expenses subject to significant day-to-day fluctuations?

- Have your planning and budgeting processes been historically accurate in forecasting financial results?

- Are adequate backup funding resources likely to be available?

- Is the governing body trying to expand the organization?

The Workgroup advises organizations to maintain a minimum reserve level of 25% of the annual expense budget, enough to cover three months’ expenditures.

Others suggest that a sensible target might be the average gap between revenues and expenses. Under this guideline, organizations with more volatile revenue or spending would require greater operating reserves. Financial advisors typically say the ideal amount for most nonprofits is six months of cash expenditures. Ultimately, the right amount for your organization will depend on its particular circumstances—no single standard applies to all.

A critical layer of protection

Operating reserves add another layer of essential insurance when you run into revenue shortfalls that could threaten your sustainability. Building reserves greatly improves your organization’s odds of continued existence.

© 2016

The New Year brings changes in payroll requirements employers must meet to avoid costly penalties. A new Form I-9 – Employment Eligibility Verification was released November 14, 2016, by the U.S. Citizenship and Immigration Service. Employers are required to complete the new Form I-9 for all employees hired after January 22, 2017. Forms that were completed for employees hired before January 22, 2017, are still in compliance. The original Form I-9 was established in 1986 to document verification of the identity and employment authorization of all new employees, both citizens and noncitizens.

The new, fillable Form I-9 is available online at www.uscis.gov/i-9. The form contains pop-up information icons and error-checking capabilities to help capture more accurate information. The new, online version will not allow mandatory fields to be left blank. It also offers an online service for answering questions with an “Ask Emma” Q & A feature.

The form is not an electronically submittable form and must still be printed, physically signed and dated by the employee and employer and retained. Both the employer and the employee must complete their respective sections of Form I-9 and, in most cases, the employer must keep the form until the latter of three years from the date of hire or one year after the date employment ended.

Penalties for employers who commit immigration-related offenses increased significantly in 2016. They range from $216 to $2,156 per individual. Avoid the penalties by correctly completing and retaining the new Form I-9 and supporting documentation.

Yeo & Yeo’s Tax Services Group has been alerted that a new email phishing scam is occurring, disguised as an alert from tax professionals like Yeo & Yeo.

The bogus emails are designed to look like they are coming from the tax professionals’ firm. The emails offer a direct link to a Tax Organizer, or

they state that a document is available to download from a portal. The email includes the recipient’s name and states that a Tax Organizer is available

or has been completed, and encourages the recipient to click on a link to an “Individual Tax Organizer – Signed.pdf.” Do not click on these malicious .PDF links.

Legitimate notices from tax professionals will direct the recipient through secure program logins and will not contain links.

Please

be alert to any such suspicious emails and, if in doubt, contact Yeo & Yeo or the purported sender directly.

Kicking off February 1, organizations around the country will support American Heart Month, and Yeo & Yeo is joining in by being casual for a cause.

Firm employees will dress in red shirts and wear jeans on Fridays throughout February. The Michigan accounting firm is proud to support the cause by

promoting and providing opportunities for firm-wide support to unite in life-saving awareness-to-action movements.

Yeo & Yeo has consistently been named one of Michigan’s Best and Brightest Companies in Wellness since 2014, an initiative that recognizes and celebrates quality and excellence in worksite health. The program highlights companies that promote a culture of wellness.

“We are committed to the health and wellness of our employees, and our goal is to help them be empowered to make real changes in their health and lifestyle behaviors,” said Thomas E. Hollerback, president and CEO of Yeo & Yeo.

Yeo & Yeo supports the wellness of its employees by providing an AED for every office and encouraging life-saving training. The Michigan accounting firm offers a gold level healthcare plan, relieving its employees of a large portion of premiums. In addition to keeping healthcare costs low, the firm has a high percentage of participation in its wellness plan which includes a further healthcare premium reduction incentive. Another initiative is the firm’s Fitbit Fitness Program. Monthly, themed challenges for individuals and teams, along with prizes and friendly competition, have resulted in a high level of involvement. The firm also provides free flu shots for all employees who elect to participate.

Please join Yeo & Yeo in recognizing American Heart Month.

Yeo & Yeo’s Construction Services group is proud to share the announcement of the Home Builders Association of Saginaw’s partnership with the Greater Michigan Construction Academy to offer Building & Construction Training in Saginaw.

The Homes Builders Association of Saginaw is proud to announce its partnership with the Greater Michigan Construction Academy to offer General Building & Construction Training in Saginaw.

Classes begin February 9th at the GMCA training facility located at: 2775 Shattuck Rd., Saginaw, MI

General Building & Construction will give the basic knowledge and principles of carpentry, masonry, concrete finishing, electrical work, HVAC, and plumbing. Students will become skilled in different phases of a project from start to finish. Once completing this course, the trainee will be able to interpret construction drawings; perform quality concrete and brickwork, frame walls, ceilings, and floors of a structure, and install the proper wiring and piping for electrical and plumbing systems. Training will also include interior and exterior finishing. The General Building & Construction program has a focus in residential construction. Presentations will be given by local home builders to share their knowledge and expertise and give insight and support to students.

“The Greater Michigan Construction Academy is excited to bring a residential building program to the Saginaw area. By partnering with the HBA we are able to reach a group of individuals who are looking to go into home building. The need for skilled labor in both commercial and residential building trades is still on the rise, and we are proud to be able to offer both in the Great Lakes Bay Region.” – Stephanie Davis, Vice President of GMCA.

Founded in 1955, The Home Builders Association of Saginaw is a professional organization providing progressive and responsive contributions to the building industry and our community. In addition to housing issues, the association seeks to protect the environment and to provide education and a better quality of life for all citizens.

“Quality and professionalism is a strength of HBA members. If we can mentor and assist students in building trades classes such as the General Building & Construction offered by GMCA, we can provide dialogue with students to support their career endeavors. The home building industry is in need of highly skilled and trained professionals. The community needs talented workers; the future of home building lays in the generations to follow.” – Michelle Revette, Executive Officer of the Home Builders Association of Saginaw.

The Home Builders Association of Saginaw (HBAS) is also proud to announce that funding can be provided for students taking this course. With the announcement of a grant, given through the National Association of Home Builders (NAHB), HBAS has the opportunity to sponsor several students entering this course, says Michelle Revette of the grant, “Our goal is to provide $10,000.00 in tuition assistance for students that want to become a part of the skilled trade workforce – building our communities. We take great pride in the hard work our members present and we are very excited to include and mentor the future builders of Saginaw County”.

You may contact 989-793-1120 if you would like to know more about this program and sponsorship for funding.

Yeo & Yeo CPAs & Business Consultants is releasing the results of the 2017 Leading Edge Alliance (LEA Global) National Manufacturing Outlook Survey.

With more than 250 participants, this survey report contains the expectations and opinions of manufacturing executives in more than 20 states across the country producing a wide variety of products including industrial/machining, transportation/automotive, construction, food and beverage, and other products.

Results from the survey include:

- 74% of small manufacturers and 69% of large manufacturers expect revenue to grow in 2017.

- Manufacturers are more optimistic about their local/regional economies than the national or global economies.

- The top priority for manufacturers in 2017 is “cutting operations costs;” however, high-growth manufacturing respondents are more focused on “research and development,” with 12% of high-growth respondents reinvesting more than 10% of annual revenue.

- Labor continues to be a challenge for manufacturers with 67% of respondents expecting labor costs to “increase” and an additional 7% expecting labor costs to “increase significantly” in 2017.

- Appropriate cost allocation and accurate and timely data will become required capabilities for successful businesses in the industry.

- More manufacturers will be considering both sales and mergers in 2017 as well as strategic acquisitions.

U.S. manufacturing industry headwinds are significant and include both internal issues, such as high inventory-to-sales ratios, the cost of technology, and labor shortages, as well as external issues like the price of raw materials and strength of the dollar.

Strategic manufacturers should have ongoing conversations with all of their advisors, including their accounting and tax provider, as to how to overcome these challenges and achieve their business goals.

“We can offer a range of solutions to manufacturers, from tax credits and entity structuring, to technology advancements and implementing operational assessments that are important for making sound business decisions,” said Yeo & Yeo Principal and Manufacturing Services Group Leader Amy Buben . “We help manufacturers align the critical operations of their companies: finance, people, processes and technology.”

Read the entire survey report, 2017 National Manufacturing Outlook and Insights – Strategies to Overcome the Headwinds, for in-depth information about the challenges the respondents face, the key strategies that the best-run manufacturers believe will be most effective, and the outlook for 2017.

The domestic production activities deduction, also known as “DPAD” or “Section 199 deduction,” is meant to encourage domestic production. This potentially valuable tax break can be used by many types of businesses, from manufacturing to farming.

Understanding the acronyms

Before trying to calculate the DPAD, it helps to understand the acronyms involved. One important factor is qualified production activities income (QPAI), which is the amount of domestic production gross receipts (DPGR) exceeding the cost of goods sold and other expenses allocable to that DPGR. Most businesses will need to allocate receipts between those that qualify as DPGR and those that do not unless less than 5 percent of receipts are not attributable to DPGR.

Farmers qualify for DPAD as producers of crops and from the sale of raised breeding, dairy or draft livestock. Apart from farming, DPGR can come from a number of activities, including the construction of real property within the United States. It also can result from the lease, rental, licensing or sale of other qualifying production property, such as machinery, office equipment or computer software. The main rule regarding any property is that it must have been manufactured, produced, grown or extracted in whole or “significantly” within the United States. While each situation is assessed on its merits, the IRS has said that, if the labor and overhead incurred in the United States accounted for at least 20 percent of the total cost of goods sold, the activity typically qualifies.

What are the limitations? The DPAD is limited to 50 percent of Form W-2 wages paid to employees and allocable to DPGR. Unfortunately, many farmers do not pay W-2 wages which disqualifies them from deducting at least 50 percent of W-2 wages under DPAD. You may be able to avoid this rule by making legitimate wage payments to family members including spouses and children over the age of 18. In addition, your farming operation may be financially stable enough to hire employees to complete tasks instead of hiring on a contract labor basis. In order to maximize your DPAD, you should ensure that 50 percent of W-2 wages reach at least 9 percent of the farm’s QPAI.

Simplifying the calculations

Although determining what costs are allocable to DPGR can get complicated, some smaller businesses can simplify their calculations. Under the Small Business Simplified Overall Method, costs are allocated between DPGR and non-DPGR based on relative gross receipts. This is the most common approach used by farmers

The Simplified Deduction Method, another method for calculating QPAI, can be used by most businesses whose assets are no more than $10 million, or whose average gross receipts do not exceed $100 million. This approach is similar to the Small Business Simplified Overall Method in that most expenses are allocated between DPGR and non-DPGR based on gross receipts. The allocation is not used for the cost of goods sold.

If your business can claim the DPAD, you may be able to deduct 9 percent from the lesser of your QPAI or taxable income. As such, it could boost your cash flow. Please contact a member of Yeo & Yeo’s Agribusiness Services Group for help with determining whether and how the deduction could work for you.

© 2015

Why do so many businesses continuously struggle to make ends meet, while others appear to thrive year after year? Why do some business owners seem to have an unlimited amount of time to take family vacations and play active roles in their communities, while others work an excessive amount of hours and are seemingly chained to their business?

One of the main differentiators between the good and the exceptional is the amount of focus and attention that the business owner gives to the big picture. It is easier, more comfortable, and often more fun to spend a majority of your time working in your business (managing and doing), as opposed to spending time working on your business (leading, creating value, holding others accountable and communicating the vision). However, the truly successful entrepreneur understands that big-picture thinking is what drives business growth and overall success.

Four Critical Factors

We all know there are many keys to success. I have worked with hundreds of business owners during my career, and have seen many successes and a few failures along the way. It is these experiences that led me to recognize four critical factors that can help take you from being a good entrepreneur to becoming an exceptional leader and business owner.

1. Know the value of your business and the drivers that affect value.

2. Focus on key performance indicators that can drive significant change throughout your organization.

3. Understand how your business and personal life support each other.

4. Create a clear vision of the future with specific, measurable objectives.

Know Your Value

Sure, everyone wants to know the value of their business if they’re looking to sell or transfer shares, or are involved in Litigation Support . However, a business valuation is a useful tool to make important decisions about the future such as estate planning, succession planning, determining life insurance needs and even looking for ways to increase value. Additionally, knowing the value of your business or, more importantly, understanding the drivers that create and sustain value, should be a key factor in your decision-making and how you manage the business. Always strive to create value for your business, and make decisions based on whether or not value is being created or damaged.

An annual review of your business value allows you the ability to track your performance in terms of estimated change in value, not just on revenue. The process of preparing a business valuation takes into account where you’ve been, where you are today, and where you appear to be heading. The main reason we are in business is to create wealth. A business valuation takes into account the entire operation and provides you the opportunity to see how your decisions affect business value.

If you’re looking to exit your business, value becomes even more critical. It has been said that you should begin planning your exit when you start your business. By understanding value drivers, and raising the value of your business, you make it more marketable. As an added bonus, many of the things that make the business more marketable also help prepare you for unforeseen events. By creating a sound business structure, employing efficient processes and growing internal talent, you are in the best position to handle whatever the future has to bring.

Know Your Numbers

I am not suggesting that you become an accounting expert. That may not play to your personal strengths and probably is not the reason you became an entrepreneur and business owner. Although it would serve you well to have a working knowledge of financial statements, it is more important that you have a thorough understanding of the key performance indicators (KPI) that drive the decision-making and day-to-day success of the business. This way, you can focus on your business while the accounting professionals take care of the details.

We continually measure things in our businesses. For many, the process of measuring data becomes an exercise in futility—we are not effectively using the results to reach strategic goals. When used correctly, the right measurements can become a vital part of the company’s strategy. The key to driving change and improving culture within the organization is to define the strategic initiatives, develop KPI to measure the progress, and create action items that lead toward achieving the desired objectives.

KPIs can provide an immediate snapshot of the overall performance of your business. Depending upon the stated objectives and the urgency of the situation, certain KPIs may be reported daily or weekly, while others may require monthly or quarterly reviews.

An added benefit of creating KPIs is that the mere act of measurement and communicating the results promotes an atmosphere of learning within the organization. The more your team understands about the key success factors of the business, the more likely they are to develop creative and efficient ways to meet the objectives.

Know Your Wealth

In most instances, your business represents your largest personal asset. However, it does not represent your entire portfolio, nor does it encompass all of your personal goals and objectives. Knowing your total net worth is important. The main reason: It is very easy to put this on the back burner as you spend time growing the business. The process of preparing a personal balance sheet forces you to take a close look at your personal financial situation and be aware of where you are on the road to where you want to be. Your personal wealth is about something of greater importance than just the business. It is about your family, your security, and your legacy. You should take a financial snapshot of where you stand at least once per year.

For many business owners, it’s easy to get so caught up in the responsibility and daily minutiae of running a successful business that they forget, or put off, the bigger picture. From a practical standpoint, you should take the time and effort to get your estate and trust documents in order, assure that you have adequate insurance in case of a catastrophe, and build for retirement apart from the business. As it relates to the business, your goal should be to maximize value by building an organization that can thrive without you. This will allow you the freedom to spend as much or as little time in the business as you desire, while creating the opportunity to pursue other interests.

The measurement and accumulation of personal wealth is important in that it provides more opportunity to pursue your dreams and provides security for your family. Success can be defined in a variety of ways, financial or otherwise, and it is important to remember that net worth does not equal self-worth. Ultimately, we all have personal goals and dreams outside of our business. It is important to keep these in the forefront and not allow them to get deferred while you work only on the business.

Know Your Future

Know your future, or at least have a vividly clear picture of what it would look like if your plans succeed. With a clear vision, decision-making becomes substantially easier, as you can focus on the important and not be sidetracked as much by the urgent or the interesting. It allows you to stay focused on the prize. Dreaming is a big part of running a business. As those dreams become a vision, the vision becomes a strategic plan. So . . . what’s your plan? What are your three to five major company initiatives that will have the greatest positive impact on the business and its value? You, and the key members of your management team, should be able to quickly identify them.

Operationally, that could mean improving cycle times, eliminating waste, or improving on-time delivery. Financially, it may mean preparing budgets, reducing outstanding debt, or reducing accounts receivable days. For marketing, maybe it’s brand awareness, digital presence, or introducing a new product or service. Or, maybe it’s R&D, customer satisfaction, inventory turns . . . you name it. Whatever will have the greatest impact on the business, it is important that you can clearly visualize the end result and assign responsibilities and accountabilities to assure that you get there.

In most cases, it’s not that the business owner doesn’t understand the importance of focusing on the big picture, it’s just that other important initiatives come up—pushing the process to the back burner. And before you know it, another year has passed, and nothing has changed.

You own your business. No one cares about the business as much as you do. No one can do this job for you. Don’t think that you have to do it alone. Securing the services of a trusted advisor could become very beneficial in the process. They will bring an outside set of eyes and experiences to the company, keep you on track, and help ensure that big-picture strategy remains a priority.

However you get there, I am confident that a sharper focus on the big picture will provide greater company value, a more engaged workforce, and more security for you and your family.

In May 2016, the U.S. Department of Labor (DOL) finalized its controversial “overtime rule,” which doubles the minimum salary an employee must receive in order to qualify for the “white collar” exemption from overtime pay. Many construction companies employ relatively low-paid managers who would have lost their exempt status under the rule, which was scheduled to take effect December 1, 2016. According to the National Association of Home Builders, approximately 100,000 construction supervisors would have been eligible for overtime under the new rule.

With just over a week before implementation of the new rules, a federal judge blocked the implementation of the rule that would have extended overtime eligibility to millions of workers across the country. With Republicans controlling both the Senate and the House and the Trump administration taking office, implementation of the new overtime rule is still up in the air. While there is uncertainty about the long-term future of this rule, it is still necessary to be aware of the impact it could have on your business.

What would change?

The final rule increases the salary threshold for exempt executive, administrative and professional (EAP) employees from $455 per week ($23,660 per year) to $913 per week ($47,476 per year). It also increases the salary threshold for highly compensated employees (HCEs) from $100,000 per year to $134,004 per year.

In determining whether an employee is exempt, up to 10% of the salary threshold may be satisfied by nondiscretionary bonuses, incentive payments or commissions, provided they are paid at least quarterly. Both salary thresholds will be adjusted automatically every three years, beginning on January 1, 2020.

What would not change?

The new rule does not change the methods of calculating overtime or (apart from the increased salary threshold) determining whether an employee is exempt from the overtime rules. Under the federal Fair Labor Standards Act (FLSA), employees generally are entitled to time-and-a-half for each hour they work in excess of 40 hours per week.

An employee qualifies for the EAP exemption if three tests are met:

- Salary basis test. The employee receives a predetermined, fixed salary that is not subject to reduction based on variations in the quality or quantity of work.

- Salary threshold test. The employee’s salary meets or exceeds a specified amount ($913 per week as of the previously planned effective date of December 1, 2016).

- Duties test. The employee’s primary job duties involve the type of work associated with exempt executive, administrative or professional employees. HCEs are subject to a less stringent duties test than other workers, which makes it easier for them to qualify as EAPs.

In the construction industry, the EAP exemption generally does not apply to nonmanagement employees who spend a significant portion of their time performing manual labor rather than supervising other workers, regardless of salary level.

How will it affect contractors?

Under the new rule, businesses with previously exempt employees who earn $455 or more per week but less than $913 per week will have to pay those employees time-and-a-half for overtime. If those employees regularly work more than 40 hours per week, the additional expense can be significant. There are several options for easing the burden of these new overtime obligations:

- Switch previously exempt employees from salaried to hourly status. Set their hourly rates so that their overall pay, taking into account estimated overtime, is comparable to what they were earning before.

- Project your compensation expense under the new rule. For employees expected to receive less than $913 per week, including overtime, consider raising their salaries to the new threshold.

- Eliminate overtime. You can do this by hiring additional workers or redistributing work among existing workers.

- Use independent contractors. These workers are not subject to overtime requirements. But keep in mind that both the DOL and the IRS have been cracking down on companies that misclassify employees as independent contractors.

When taking steps to mitigate the impact of the new overtime rule, don’t forget to consider employee morale. For example, formerly exempt employees switched from salaried to hourly pay may view the change as a demotion or loss of status—even if their take-home pay is the same as or higher than before.

Even if you continue to pay salaries, the loss of exempt status may not sit well with some staff members. Also, employees will have to track all of their hours to be sure they are compensated for overtime and may lose some of the flexibility associated with exempt status.

Where to begin?

Start analyzing your compensation program and evaluating the potential financial impact of the overtime rule now. Whichever strategy you choose to deal with it, develop a communications strategy to inform employees of your decisions and address employee morale issues.

© 2016

The core of any organization’s fraud prevention program is strong internal controls. Yet too many governments either fail to develop controls that address common risks or, if they establish controls, neglect to enforce them. Your government must do both if it wants to help prevent occupational theft and fraud perpetrated by outsiders.

Governments at risk

According to the Association of Certified Fraud Examiners (ACFE), corruption, billing fraud and payroll fraud are three of the most frequent types of fraud schemes within government administration. However, proper segregation of duties — for example, assigning account reconciliation and fund depositing to two different staff members — is a relatively easy and effective method of preventing such fraud.

For all government entities of any size, such controls as strong management oversight, regular audits and confidential fraud hotlines are associated with decreases in financial losses. The ACFE has found that proactive data monitoring and analysis is the most effective means of limiting the duration and cost of fraud schemes — 50% shorter and 60% smaller than organizations that do not monitor data.

Getting priorities straight

Most governments have at least a fundamental set of controls, but employees bent on fraud can usually find gaps in the fence. Government entities handle large amounts of money and are involved in a significant number of transactions, which make them a prime target for fraud. This can be especially problematic when the “tone at the top” is lax and management or board members indicate that preventing fraud is low on their priority list. Most governments do not have funds budgeted to combat fraud.

Government boards may also inadvertently enable fraud when they place too much trust in the manager and fail to challenge that person’s financial representations. Unlike for-profit companies, government boards may lack members with financial oversight experience, which means they may fail to notice important warning signs that something is amiss.

Send the right message

How municipalities deal with perpetrators can also increase their fraud risk. A reputation for honesty and fiscal responsibility is any government entity’s bedrock. So it is not surprising that many organizations choose to quietly fire fraud perpetrators and sweep such incidents under the rug.

Unfortunately, such actions encourage fraud by telling potential thieves that the consequences of getting caught are relatively minor. Even if an incident is hushed up, it could fuel insidious rumors that do more reputational damage than publicly addressing the issue head-on would. It is better, therefore, to file a police report, consult an attorney and inform major stakeholders about the incident and what you are doing to prevent it from happening again.

Cover all bases

Internal control policies should address both common fraud risks and those specific to your organization and constituents. Is your government entity exposed to fraud? Answer the questions on Yeo & Yeo’s Internal Control Checklist to find out.

© 2016

Unfortunately, divorce often becomes acrimonious, and that acrimony frequently centers on money. Allegations of hidden assets, or even fraud, can muddy the waters and heighten tension, making a fair resolution increasingly difficult. Especially when a private business interest is involved, valuation and forensic accounting expertise is key in helping spouses equitably divide their assets.

Looking behind the numbers

Valuators may have to watch out (and adjust) for spouses trying to dissipate their businesses’ values. For instance, the moneyed spouse may attempt to hide business assets, delay revenue recognition, or overstate expenses.

The non-moneyed spouse generally has less experience and knowledge of the business, as well as limited access to the business records, and therefore would be less likely to detect this course of action. To determine whether the claim is justified or is completely without merit, valuation and forensic accounting expertise can be key.

A lower bottom line benefits a moneyed spouse in two ways. First, to the extent that a company’s value is based on its earnings and adjusted net cash flow, reduced income lowers value. Therefore, low profits increase a moneyed spouse’s share of the marital estate’s remaining assets. Some moneyed spouses will even hide physical assets or use fraudulent accounting tactics to lower profits reported before their divorces.

This requires the valuation expert to look behind the numbers and use forensic accounting techniques to search for unreported income. One approach valuators use to uncover missing income is to search for hidden cash.

Finding missing cash

Business owners sometimes receive unreported income in the form of cash. To avoid detection, the business does not record the income in its books or deposit the cash in its bank account. However, professionals can use several forensic accounting techniques to indicate whether cash is missing and estimate how much the owner is not reporting.

Under the bank deposits method, the expert reconstructs income by analyzing bank deposits, canceled checks, and currency transactions. The expert also accounts for cash payments made from undeposited currency receipts as well as non-income sources of cash such as loans, gifts, inheritances or insurance proceeds.

Alternatively, when professionals use the source and funds application method, they analyze the business owner’s personal sources and uses of cash. This method is effective in addressing the question: Where did income and other funds come from, and what were they used for? If the owner is spending more than he or she is taking in, the excess represents unreported income.

The net worth method is based on the assumption that an unsubstantiated increase in a business owner’s net worth is attributable to unreported income. Here, the valuator estimates net worth using documents such as bank and brokerage statements, real estate records, and loan or credit card applications.

Under the percentage markup method, the expert estimates net income by applying a benchmark profit percentage to sales or some other base amount. He or she starts with the amount of gain in net worth, subtracts reported income and adjusts this amount to reflect nondeductible expenditures—such as capital asset acquisitions—and non-income sources of funds. This method is often used to corroborate results of other methods.

Reaching an accurate and fair result

The techniques described here are just a few examples of the many ways forensic accounting techniques can produce more accurate valuations. When searching for hidden cash, it is important for valuation professionals and legal counsel to work together closely, because laws and legal precedents in divorce cases may differ from state to state. Such collaboration can help ensure that the numbers are accurate—and that settlements are fair and hold up in court.

© 2016

Tammy Moncrief, CPA, has been elected to the Yeo & Yeo CPAs & Business Consultants board of directors, and Peter J. Bender, CPA, CFP® has been reelected to the firm’s board of directors effective January 1, 2017, announced Thomas E. Hollerback, president and CEO. They will serve two-year terms.

Tammy Moncrief, managing principal of the Auburn Hills office, is a member of the firm’s Tax Services Group. She has 29 years of public accounting experience. Her areas of expertise include business consulting, tax planning and preparation, multi-state taxation, and trust and estate planning with a strong emphasis on professional service firms, as well as the real estate, construction, healthcare, engineering, agribusiness, and wholesale sales and distribution sectors. She is vice-chair of the Michigan Association of Certified Public Accountants’ Federal Tax Task Force. In our community, Moncrief is an active volunteer for the University of Detroit Jesuit High School and is past president of the Michigan State University Detroit Area Development Council. She has held positions with the finance committee for Notre Dame Preparatory High School. She volunteers for activities and has held various committee chair positions for the Academy of the Sacred Heart.

Peter Bender is a principal and a member of the firm’s Agribusiness, Employee Benefits and Estate Planning Groups. He has 28 years of experience in auditing, and tax planning and preparation for businesses and individuals, with a concentration on agribusinesses. He also performs audits for employee benefit plans. Bender is chairman of the Michigan Association of Certified Public Accountants’ Agribusiness Task Force. He is a Certified Financial Planner™ and a member of the Financial Planning Association. In our community, Bender is chairman of the board of the Frankenmuth Credit Union and serves on the board for Wellspring Lutheran Services. He is a member and past president of the Saginaw Rotary Club, and a member of the Valley Lutheran High School Growing Campaign Cabinet and the St. Lorenz Foundation Finance Committee. He is based in the firm’s Saginaw office. Check the background of Pete Bender on FINRA’s BrokerCheck.

Yeo & Yeo’s Tax Services Group is pleased to provide updated tax calendars for your use. Please refer to Yeo & Yeo’s 2017 Tax Calendar for Businesses and 2017 Tax Calendar for Individuals and Trusts.

The revised calendars reflect a recent change whereby the IRS provided a 30-day extension of the due date for Affordable Care Act information that must be reported to covered individuals and employees, from January 31, 2017, to March 2, 2017. This

includes IRS Forms 1095-B (Health Coverage) and 1095-C (Employer-provided Health Insurance Offer and Coverage).

The calendars also reflect other updates such as the due date for federal tax returns, which this year is Tuesday, April 18. The

Emancipation Day holiday is being observed in Washington D.C. on Monday, April 17, so Tax Day is the following day.

Contact us to ensure you are meeting all applicable deadlines. For other helpful tools, visit the Tax Center at yeoandyeo.com.

- Example 1: You have a separate shelving unit in your basement that holds boxes of inventory. This space used exclusively for your business may be included when determining your home office deduction.

- Example 2: You have some clothing and purses that you have listed on eBay that are kept in your closet, interspersed with your own personal items. This would not be exclusive use and this area could not be used as part of your home office deduction calculation; however, if you were to amass several items into an area of your closet, exclusive for items you are selling, this section of the closet could qualify.

Home office deductions are limited by the amount of associated home business income—in other words, you cannot use the home office deduction to put you into a net taxable loss, but you can use it to bring your home business income to zero. There is a simplified method and a non-simplified method for calculating the deduction, and the IRS allows taxpayers to choose annually whichever method they prefer.

- The simplified method is easier to work with; however, it is limited to 300 square feet of designated space and any unused portion cannot be carried forward to the next tax year.

- The non-simplified method is based on the percentage of the home used for business purposes and it incorporates utilities, real estate taxes and home insurance into the computation. The record-keeping and calculations are more complex, and tracking depreciation and basis is also required, but using this method allows a taxpayer to carry forward unused portions of the deduction into a year where there is sufficient income to utilize it.

Proper planning and documentation is key to the optimum tax treatment. Please let me know if you would like me to assist you with your home office deduction or any other tax matters.

The core of any organization’s fraud prevention program is strong internal controls. Yet too many nonprofits either fail to develop controls that address common risks or, if they establish controls, neglect to enforce them. Your nonprofit must do both if it wants to help prevent occupational theft and fraud perpetrated by outsiders.

Charities at risk

According to the Association of Certified Fraud Examiners (ACFE), billing fraud, check tampering and expense reimbursement fraud are the three most common types of employee theft found in religious, charitable and social service organizations. Theft of cash or minor supplies is often a common occurrence as well. However, proper segregation of duties — for example, assigning account reconciliation and fund depositing to two different staff members or prohibiting a check writer to also be a check signer — is a relatively easy and effective method of preventing such fraud.

For all types of organizations, such controls as strong management oversight, regular audits and an engaged board or finance committee are associated with decreases in financial losses. The ACFE has found that proactive data monitoring and analysis is the most effective means of limiting the duration and cost of fraud schemes — 50% shorter and 60% smaller than organizations that do not monitor data.

Getting priorities straight

Most nonprofits have at least a rudimentary set of controls, but employees bent on fraud can usually find gaps in the fence. For example, charities tend to devote the lion’s share of their budgets to programming and can be stingy about allocating dollars to enforcing internal controls and administrative duties. This can be especially problematic when the “tone at the top” is lax and executive directors or board members indicate that preventing fraud is low on their priority list.

Nonprofit boards may also inadvertently enable fraud when they place too much trust in the key management staff and fail to challenge that person’s financial representations. Unlike for-profit companies, nonprofit boards may lack members with financial oversight experience, which means they may fail to notice important warning signs that something is amiss.

Trust is an Achilles’ heel throughout many nonprofits. Organizations often regard their staff members as family and skip such important fraud prevention measures as conducting background checks. In many cases, managers are allowed to override internal controls without recourse and volunteers are trusted to accept cash donations or keep the books without the oversight of a staff member — both very risky activities.

Send the right message

How nonprofits deal with perpetrators can also increase their fraud risk. A reputation for honesty and fiscal responsibility is any charity’s bedrock. So it is not surprising that many organizations choose to quietly fire fraud perpetrators and sweep such incidents under the rug.

Unfortunately, such actions encourage fraud by telling potential thieves that the consequences of getting caught are relatively minor or low risk. Even if an incident is hushed up, it could do more reputational damage if discovered than publicly addressing the issue head-on would. It is better, therefore, to file a police report, consult an attorney and inform major stakeholders about the incident and what you are doing to prevent it from happening again. This proactive measure sends a clear message that you are working to safeguard the organization’s assets and continue the charitable mission.

Cover all bases

Internal control policies should address both common fraud risks and those specific to your organization and constituents. Is your nonprofit exposed to fraud? Answer the questions in Yeo & Yeo’s Internal Control Checklist to find out. Contact Yeo & Yeo for more information about internal controls.

© 2016

Yeo & Yeo CPAs & Business Consultants is pleased to announce Michael A. Georges, CPA, as the leader of the firm’s Nonprofit Services Group. He will lead the strategic direction and management of the firm’s state-wide Group, and oversee the Group’s business development, training and staff development.

Georges is a principal with more than 30 years of public accounting experience, and a passion for working with nonprofits. His areas of expertise include tax planning and preparation for individuals, businesses and nonprofit organizations, as well as audit services for the government, education and nonprofit sectors. He is also a member of the firm’s Tax Services Group and the Education Services Group.

“Mike serves many nonprofit clients and has an immense amount of tax, audit and consulting experience,” says David Youngstrom, principal and the firm’s Audit Service Line Leader. “He strengthens the Group with his ability to train, advise and guide the firm’s nonprofit clients in the financial aspects of running a successful nonprofit.”

Georges is a member of Michigan School Business Officials. He is based in the firm’s Ann Arbor office. In addition to his work at Yeo & Yeo, Georges serves on the board of directors of the Grosse Ile Educational Foundation and the board of directors of Child’s Hope Child Abuse Prevention Council of OutWayne.

The 21st Century Cures Act, which was signed into law December 13 primarily to fund medical research, also included provisions that allow small employers to provide Health Reimbursement Arrangements (HRAs) to employees. This means that for tax years beginning after December 31, 2016, small employers may establish a plan to reimburse employees for out-of-pocket medical expenses and/or health insurance premiums. These reimbursements are deductible to the small employer, but generally are not taxable to employees.

A “Qualified Small Employer HRA” must meet the following requirements:

- Employer must employ fewer than 50 full-time employees.

- Employer may not offer a group health plan to any of its employees.

- Reimbursements must be made on the same terms for all employees (though employees under age 25, part-time or seasonal, under a collective bargaining agreement or employees with fewer than 90 days of service may be excluded).

- Must be funded by the employer (no salary reduction contributions).

- Employees must provide proof of health insurance coverage in order to be eligible to participate.

- Reimbursement plans for individuals may not exceed $4,950 per year, while plans allowing for reimbursement for all family members are capped at $10,000. This amount will be subject to annual cost-of-living adjustments. For arrangements in force for less than a 12-month period, these amounts are prorated.

In order to participate in an HRA, employers must provide notice to employees explaining the employees’ permitted benefits under the arrangement and the employees’ responsibility to maintain minimum essential healthcare coverage. Verbiage also must include information for employees applying for tax credits on any governmental health exchange. This employee notice is due 90 days before the beginning of the plan year, but due to the timing of the passage 100c of the Act, this has been extended to March 13, 2017, for this year only.

Please contact us if you would like us to assist you in determining whether a Health Reimbursement Arrangement is right for your business or organization.

Take a moment and think about all of the security features that are used to keep your organization’s network safe. Passwords and firewalls help keep the bad guys away from your vital information. But all of these security measures don’t mean a thing if someone clicks on a malware link inside an email.

As phishing attacks have grown, so too has the emphasis on Cybersecurity. In fact, according to the recent IBM X-Force Research’s 2016 cybersecurity Intelligence Index, the manufacturing sector is now one of the most frequently hacked industries, second only to healthcare. A tool that many are using to help prevent cyberattacks within their organization is security awareness training as a way to educate employees. Having knowledge of malware and phishing is as important as having proper antivirus and firewall protection.

How does security awareness training work?

A security awareness training provider will begin the training process with an email exposure check that shows which email addresses within an organization’s domain are being exposed to spear-phishing attacks on the Internet. This service looks deep into websites, Word, Excel and PDF files that are on the Internet. By performing these tests, business owners and managers can see which employees are the most susceptible to phishing emails. Training modules soon follow to teach employees what to look for.

Statistics show that it works

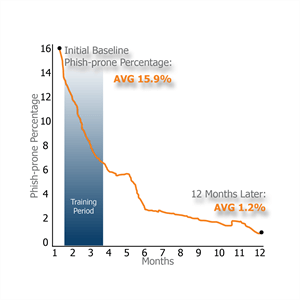

Security awareness training helps turn your employees into your organization’s first firewall. Through training, employees become the best defense you can have. We aggregated the numbers and the overall Phish-prone percentage dropped from an average of 15.9 percent to an amazing 1.2 percent in just 12 months. The combination of web-based training and frequently simulated phishing attacks really works.

Manufacturing is a target too

Cybersecurity continues to be a concern in the manufacturing industry. In the Verizon 2016 Data Breach Investigations Report, the manufacturing industry is listed as a top target of cyber-espionage. Cyber-espionage features external hacking threats that infiltrate victim networks seeking sensitive internal data and trade secrets. The tactics used by hackers to gain information through cyber-espionage begins with phishing and malware. For hackers, phishing is the most efficient way to get the information they want to hold for ransom.

Manufacturing companies are urged to do their research and perform the following to help mitigate cyber-attacks:

- Perform an annual IT risk assessment to see where threats are coming from.

- Use penetration testing to simulate threats.

- Conduct vulnerability scans throughout the year and stay updated on new threats.

It’s important to remember that everyone is a target of phishing attacks. These attacks happen every day, but the good news is they can be prevented. Proper training is great a great way to prevent attacks, but equally important is having a proper backup and disaster recovery plan in place. Nothing is bullet-proof in IT, but being prepared for any circumstance can help save money and downtime in the event of a disaster.

For more information about security awareness training, contact your Yeo & Yeo advisor or Jeff McCulloch, President of Yeo & Yeo Technology, jefmcc@yeoandyeo.com or 800.607.1446.

Here are some of the key tax-related deadlines affecting businesses and other employers during the first quarter of 2017. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

January 31

- File 2016 Forms W-2, “Wage and Tax Statement,” with the Social Security Administration and provide copies to your employees.

- File 2016 Forms 1099-MISC, “Miscellaneous Income,” reporting nonemployee compensation payments in Box 7 with the IRS, and provide copies to recipients.

- File Form 941, “Employer’s Quarterly Federal Tax Return,” to report Medicare, Social Security and income taxes withheld in the fourth quarter of 2016. If your tax liability is less than $2,500, you can pay it in full with a timely filed return. If you deposited the tax for the quarter in full and on time, you have until February 10 to file the return. Employers that have an estimated annual employment tax liability of $1,000 or less may be eligible to file Form 944,“Employer’s Annual Federal Tax Return.”

- File Form 940, “Employer’s Annual Federal Unemployment (FUTA) Tax Return,” for 2016. If your undeposited tax is $500 or less, you can either pay it with your return or deposit it. If it’s more than $500, you must deposit it. However, if you deposited the tax for the year in full and on time, you have until February 10 to file the return.

- File Form 945, “Annual Return of Withheld Federal Income Tax,” for 2016 to report income tax withheld on all nonpayroll items, including backup withholding and withholding on accounts such as pensions, annuities and IRAs. If your tax liability is less than $2,500, you can pay it in full with a timely filed return. If you deposited the tax for the year in full and on time, you have until February 10 to file the return.

February 28

File 2016 Forms 1099-MISC with the IRS and provide copies to recipients. (Note that Forms 1099-MISC reporting nonemployee compensation in Box 7 must be filed by January 31, beginning with 2016 forms filed in 2017.)

March 15

If a calendar-year partnership or S corporation, file or extend your 2016 tax return. If the return isn’t extended, this is also the last day to make 2016 contributions to pension and profit-sharing plans.

© 2016