What School Districts Need to Prepare Now for GASB 87 – Leases

Background

It is here – GASB Statement No. 87, Leases. This GASB must be implemented in school districts’ June 30, 2022, financial statements. The objective of the new GASB is to improve accounting and financial reporting for leases. Another objective is to increase financial statements’ usefulness by recognizing certain lease assets and liabilities for leases that were previously classified as operating leases and recognized as inflows or outflows of resources based on the contract’s payment provisions. GASB 87 requires a lessee to recognize a lease liability and an intangible right-to-use lease asset. A lessor must recognize a lease receivable and a deferred inflow of resources.

What to do now

Get lease information ready, amend the fiscal year 2021-22 budget for any new current year leases (exceeding one year), and make journal entries for leases before closing out the current fiscal year.

Information to collect

For current leases:

- Lease description

- Original lease term

- Any renewal options, and the determination of the likelihood of utilizing those options

- Components of the payments (fixed, variable, interest rate)

- Who has the right to terminate the lease

- Lease obligation maturities for the next five years and beyond (similar to debt maturity schedule)

Practical hint: Short-term (less than one year) leases will be recorded as operating leases had been. Leases over one year will be recorded on district-wide financials, and in the year of inception, the lease will be recorded on the fund level statements.

How to Calculate

Leases (where the district is the lessee) existing prior to 7/1/21 (before this fiscal year)

- Calculate lease liability as of 7/1/21. This will be the right-of-use asset and liability for district-wide beginning balances.

- This will not change fund level statements.

Leases existing after 7/1/21 (in this fiscal year)

- Calculate the right-of-use asset/lease liability. Practical hint: Total cost of leased equipment (as if a “capital lease”).

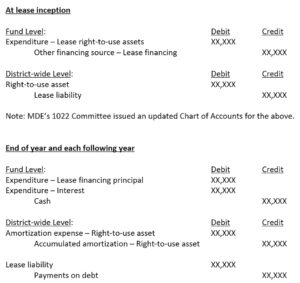

- Fund level: In the current fiscal year ending June 30, 2022 – this will be included as a:

- Revenue: Other financing sources – lease financing

- Expenditure: Lease right-to-use assets (capital outlay)

- URGENT: Include Revenue and Expenditure amounts in final budget amendments for the current fiscal year (ending June 30, 2022).

- District-wide level: In the current fiscal year ending June 30, 2022 – this will be included as:

- Asset: Right-to-use assets

- Liability: Lease liability

Leases (where the district is the lessor)

- Calculate lease receivable as of 6/30/2022. This will be recorded as an Account Receivable and Deferred inflow.

- This will change fund level statements. It will be on both the district-wide and governmental fund statements.

For the fiscal year 2022-23 and beyond, maintain the above list of information on leases. Work with your auditor, if necessary, to determine which leases require the underlying asset to be recorded as a right-to-use asset and include such leases in budgets going forward.

Journal Entries

Are you a charitably minded individual who is also taking distributions from a traditional IRA? You may want to consider the tax advantages of making a cash donation to an IRS-approved charity out of your IRA.

When distributions are taken directly out of traditional IRAs, federal income tax of up to 37% in 2022 will have to be paid. State income taxes may also be owed.

Qualified charitable distributions

One popular way to transfer IRA assets to charity is via a tax provision that allows IRA owners who are age 70½ or older to direct up to $100,000 per year of their IRA distributions to charity. These distributions are known as qualified charitable distributions (QCDs). The money given to charity counts toward your required minimum distributions (RMDs) but doesn’t increase your adjusted gross income (AGI) or generate a tax bill.

Keeping the donation out of your AGI may be important for several reasons. Here are some of them:

- It can help you qualify for other tax breaks. For example, having a lower AGI can reduce the threshold for deducting medical expenses, which are only deductible to the extent they exceed 7.5% of AGI.

- You can avoid rules that can cause some or all of your Social Security benefits to be taxed and some or all of your investment income to be hit with the 3.8% net investment income tax.

- It can help you avoid a high-income surcharge for Medicare Part B and Part D premiums, which kick in if AGI is over certain levels.

- The distributions going to the charity won’t be subject to federal estate tax and generally won’t be subject to state death taxes.

Important points: You can’t claim a charitable contribution deduction for a QCD not included in your income. Also keep in mind that the age after which you must begin taking RMDs is 72, but the age you can begin making QCDs is 70½.

To benefit from a QCD for 2022, you must arrange for a distribution to be paid directly from the IRA to a qualified charity by December 31, 2022. You can use QCDs to satisfy all or part of the amount of your RMDs from your IRA. For example, if your 2022 RMDs are $10,000, and you make a $5,000 QCD for 2022, you have to withdraw another $5,000 to satisfy your 2022 RMDs.

Other rules and limits may apply. Want more information? Contact us to see whether this strategy would be beneficial in your situation.

© 2022

Businesses should be aware that they may be responsible for issuing more information reporting forms for 2022 because more workers may fall into the required range of income to be reported. Beginning this year, the threshold has dropped significantly for the filing of Form 1099-K, “Payment Card and Third-Party Network Transactions.” Businesses and workers in certain industries may receive more of these forms and some people may even get them based on personal transactions.

Background of the change

Banks and online payment networks — payment settlement entities (PSEs) or third-party settlement organizations (TPSOs) — must report payments in a trade or business to the IRS and recipients. This is done on Form 1099-K. These entities include Venmo and CashApp, as well as gig economy facilitators such as Uber and TaskRabbit.

A 2021 law dropped the minimum threshold for PSEs to file Form 1099-K for a taxpayer from $20,000 of reportable payments made to the taxpayer and 200 transactions to $600 (the same threshold applicable to other Forms 1099) starting in 2022. The lower threshold for filing 1099-K forms means many participants in the gig economy will be getting the forms for the first time.

Members of Congress have introduced bills to raise the threshold back to $20,000 and 200 transactions, but there’s no guarantee that they’ll pass. In addition, taxpayers should generally be reporting income from their side employment engagements, whether it’s reported to the IRS or not. For example, freelancers who make money creating products for an Etsy business or driving for Uber should have been paying taxes all along. However, Congress and the IRS have said this responsibility is often ignored. In some cases, taxpayers may not even be aware that income from these sources is taxable.

Some taxpayers may first notice this change when they receive their Forms 1099-K in January 2023. However, businesses should be preparing during 2022 to minimize the tax consequences of the gross amount of Form 1099-K reportable payments.

What to do now

Taxpayers should be reviewing gig and other reportable activities. Make sure payments are being recorded accurately. Payments received in a trade or business should be reported in full so that workers can withhold and pay taxes accordingly.

If you receive income from certain activities, you may want to increase your tax withholding or, if necessary, make estimated tax payments or larger payments to avoid penalties.

Separate personal payments and track deductions

Taxpayers should separate taxable gross receipts received through a PSE that are income from personal expenses, such as splitting the check at a restaurant or giving a gift. PSEs can’t necessarily distinguish between personal expenses and business payments, so taxpayers should maintain separate accounts for each type of payment.

Keep in mind that taxpayers who haven’t been reporting all income from gig work may not have been documenting all deductions. They should start doing so now to minimize the taxable income recognized due to the gross receipts reported on Form 1099-K. The IRS is likely to take the position that all of a taxpayer’s gross receipts reported on Form 1099-K are income and won’t allow deductions unless the taxpayer substantiates them. Deductions will vary based on the nature of the taxpayer’s work.

Contact us if you have questions about your Form 1099-K responsibilities.

© 2022

When creating forward-looking financials, you generally have two options under AICPA Attestation Standards Section 301, Financial Forecasts and Projections:

1. Forecast. Prospective financial statements that present, to the best of the responsible party’s knowledge and belief, an entity’s expected financial position, results of operations and cash flows. A financial forecast is based on the responsible party’s assumptions reflecting the conditions it expects to exist and the course of action it expects to take.

2. Projection. Prospective financial statements that present, to the best of the responsible party’s knowledge and belief, given one or more hypothetical assumptions, an entity’s expected financial position, results of operations and cash flows. A financial projection is sometimes prepared to present one or more hypothetical courses of action for evaluation, as in response to a question such as, “What would happen if … ?”

Subtle difference

The terms “forecast” and “projection” are sometimes used interchangeably. But there’s a noteworthy distinction, a forecast represents expected results based on the expected course of action. These are the most common type of prospective reports for companies with steady historical performance that plan to maintain the status quo.

On the flip side, a projection estimates the company’s expected results based on various hypothetical situations that may or may not occur. These statements are typically used when management is uncertain whether performance targets will be met. So, they may be appropriate for start-ups or when evaluating results over a longer period because there’s a good chance that customer demand or market conditions could change over time.

Critical components

Regardless of whether you opt for a forecast or projection, the report will generally be organized using the same format as your financial statements with an income statement, balance sheet and cash flow statement. Most prospective statements conclude with a statement of key assumptions that underlie the numbers. Many assumptions are driven by your company’s historical financial statements, along with a detailed sales budget for the year.

Instead of relying on static forecasts or projections — which can quickly become outdated in a volatile marketplace — some companies now use rolling 12-month versions that are adaptable and look beyond year end. This helps you identify and respond to weaknesses in your assumptions, as well as unexpected changes in the marketplace. For example, a manufacturer that experiences a shortage of raw materials could experience an unexpected drop in sales until conditions improve. If the company maintains a rolling forecast, it would be able to revise its plans for such a temporary disruption.

Contact us

Planning for the future is an important part of running a successful business. While no forecast or projection will be 100% accurate in these uncertain times, we can help you evaluate the alternatives for issuing prospective financial statements and offer fresh, objective insights about what may lie ahead for your business.

© 2022

Taking care of an elderly parent or grandparent may provide more than just personal satisfaction. You could also be eligible for tax breaks. Here’s a rundown of some of them.

1. Medical expenses. If the individual qualifies as your “medical dependent,” and you itemize deductions on your tax return, you can include any medical expenses you incur for the individual along with your own when determining your medical deduction. The test for determining whether an individual qualifies as your “medical dependent” is less stringent than that used to determine whether an individual is your “dependent,” which is discussed below. In general, an individual qualifies as a medical dependent if you provide over 50% of his or her support, including medical costs.

However, bear in mind that medical expenses are deductible only to the extent they exceed 7.5% of your adjusted gross income (AGI).

The costs of qualified long-term care services required by a chronically ill individual and eligible long-term care insurance premiums are included in the definition of deductible medical expenses. There’s an annual cap on the amount of premiums that can be deducted. The cap is based on age, going as high as $5,640 for 2022 for an individual over 70.

2. Filing status. If you aren’t married, you may qualify for “head of household” status by virtue of the individual you’re caring for. You can claim this status if:

- The person you’re caring for lives in your household,

- You cover more than half the household costs,

- The person qualifies as your “dependent,” and

- The person is a relative.

If the person you’re caring for is your parent, the person doesn’t need to live with you, so long as you provide more than half of the person’s household costs and the person qualifies as your dependent. A head of household has a higher standard deduction and lower tax rates than a single filer.

3. Tests for determining whether your loved one is a “dependent.” Dependency exemptions are suspended (or disallowed) for 2018–2025. Even though the dependency exemption is currently suspended, the dependencytests still apply when it comes to determining whether a taxpayer is entitled to various other tax benefits, such as head-of-household filing status.

For an individual to qualify as your “dependent,” the following must be true for the tax year at issue:

- You must provide more than 50% of the individual’s support costs,

- The individual must either live with you or be related,

- The individual must not have gross income in excess of an inflation-adjusted exemption amount,

- The individual can’t file a joint return for the year, and

- The individual must be a U.S. citizen or a resident of the U.S., Canada or Mexico.

4. Dependent care credit. If the cared-for individual qualifies as your dependent, lives with you, and physically or mentally can’t take care of him- or herself, you may qualify for the dependent care credit for costs you incur for the individual’s care to enable you and your spouse to go to work.

Contact us if you’d like to further discuss the tax aspects of financially supporting and caring for an elderly relative.

© 2022

At Yeo & Yeo CPAs & Business Consultants, we take pride in creating an environment that challenges, supports and rewards our employees. We are family-focused, community-driven and relationship-oriented. And we love to see our employees grow and succeed.

We are honored to have been named one of West Michigan’s Best and Brightest Companies to Work For for the eighteenth consecutive year. The Best and Brightest programs identify, recognize and celebrate organizations that exemplify Better Business. Richer Lives. Stronger Communities.

Yeo & Yeo is proud of the environment we have created for our employees. We offer an award-winning CPA certification bonus program, gold standard benefits, and hybrid and remote work capabilities. Our West Michigan staff shared five reasons why our firm is such a great place to work:

- Empowerment: “In my second year as a partner, I was allowed to lead the firm’s Tax Service Line. I am grateful for the trust the firm’s leadership placed in me, especially as a younger professional at the time. As a firm, we empower our employees to lead and give them opportunities for growth and development throughout their careers.” – David Jewell, CPA, Managing Principal

- Flexibility: “One of the things I appreciate about Yeo & Yeo is that the company recognizes that each employee is different, and is willing to be flexible to accommodate each employee’s needs. We don’t have a set work schedule that everyone has to adhere to, and we are encouraged to find a path within the company that works for us and what we want to accomplish.” – Megan Taylor, CPA, Manager

- Family-focused: “I appreciate that we’re given the respect and autonomy to have flexible work schedules. We’re trusted to complete the work and given opportunities to enjoy a rewarding career without compromising on personal, family time.” – Chelsea Meyer, CPA, Manager

- Relationships: “We are not a big four firm. Everyone is not just a number. We really help each other on an individual level. We feel like we are a family. It doesn’t matter where you sit. We all work together.” – Michael Oliphant, CPA, CVA, Principal

- People first: “Yeo & Yeo treats you well. As a first-year principal, I can wholeheartedly say that the decisions the partner group makes are always in the best interest of the employees. They listen and respond. They work hard every day to create an inclusive and supportive environment. I am lucky to be around such a great group of professionals.” – Michael Evrard, CPA, Principal

What will your story be? Apply today to write the next chapter in your career.

The IRS recently released guidance providing the 2023 inflation-adjusted amounts for Health Savings Accounts (HSAs). High inflation rates will result in next year’s amounts being increased more than they have been in recent years.

HSA basics

An HSA is a trust created or organized exclusively for the purpose of paying the “qualified medical expenses” of an “account beneficiary.” An HSA can only be established for the benefit of an “eligible individual” who is covered under a “high deductible health plan.” In addition, a participant can’t be enrolled in Medicare or have other health coverage (exceptions include dental, vision, long-term care, accident and specific disease insurance).

A high deductible health plan (HDHP) is generally a plan with an annual deductible that isn’t less than $1,000 for self-only coverage and $2,000 for family coverage. In addition, the sum of the annual deductible and other annual out-of-pocket expenses required to be paid under the plan for covered benefits (but not for premiums) can’t exceed $5,000 for self-only coverage, and $10,000 for family coverage.

Within specified dollar limits, an above-the-line tax deduction is allowed for an individual’s contribution to an HSA. This annual contribution limitation and the annual deductible and out-of-pocket expenses under the tax code are adjusted annually for inflation.

Inflation adjustments for next year

In Revenue Procedure 2022-24, the IRS released the 2023 inflation-adjusted figures for contributions to HSAs, which are as follows:

Annual contribution limitation. For calendar year 2023, the annual contribution limitation for an individual with self-only coverage under an HDHP will be $3,850. For an individual with family coverage, the amount will be $7,750. This is up from $3,650 and $7,300, respectively, for 2022.

In addition, for both 2022 and 2023, there’s a $1,000 catch-up contribution amount for those who are age 55 and older at the end of the tax year.

High deductible health plan defined. For calendar year 2023, an HDHP will be a health plan with an annual deductible that isn’t less than $1,500 for self-only coverage or $3,000 for family coverage (these amounts are $1,400 and $2,800 for 2022). In addition, annual out-of-pocket expenses (deductibles, co-payments, and other amounts, but not premiums) won’t be able to exceed $7,500 for self-only coverage or $15,000 for family coverage (up from $7,050 and $14,100, respectively, for 2022).

Reap the rewards

There are a variety of benefits to HSAs. Contributions to the accounts are made on a pre-tax basis. The money can accumulate tax free year after year and can be withdrawn tax free to pay for a variety of medical expenses such as doctor visits, prescriptions, chiropractic care and premiums for long-term care insurance. In addition, an HSA is “portable.” It stays with an account holder if he or she changes employers or leaves the workforce. If you have questions about HSAs at your business, contact your employee benefits and tax advisors.

© 2022

Maintaining the status quo in today’s volatile marketplace can be risky. To succeed, businesses need to “level up” by being proactive and adaptable. But some managers may be unsure where to start or they’re simply out of new ideas.

Fortunately, when audited financial statements are delivered, they’re accompanied by a management letter that suggests ways to maximize your company’s efficiency and minimize its risk. These letters may contain fresh, external perspectives and creative solutions to manage supply chain shortages, inflationary pressures and other current developments.

Auditing standards

Under Generally Accepted Auditing Standards, auditors must communicate in writing about material weaknesses or significant deficiencies in internal controls that are discovered during audit fieldwork. A material weakness is defined as “a deficiency, or combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis.”

Significant deficiencies are generally considered less severe than material weaknesses. A significant deficiency is “a deficiency, or a combination of deficiencies, in internal control that is … important enough to merit attention by those charged with governance.”

Auditors may unearth less severe weaknesses and operating inefficiencies during the course of an audit. Although reporting these items is optional, they’re often included in the management letter. The write-up for each deficiency includes an observation (including a cause, if observed), financial and qualitative impacts, and a recommended course of action.

From compliance to business improvement

Audits should be more than just an exercise in compliance. Management letters summarize lessons learned during audit fieldwork on how to improve various aspects of the company’s operations.

For example, a management letter might report a significant increase in the average accounts receivable collection period from the prior year. Then the letter might provide cost-effective suggestions on how to expedite collections, such as implementing early-bird discounts and using electronic payment systems to enable real-time invoices and online payment. Finally, the letter might explain how improved collections would potentially boost operating cash flow and decrease write-offs for bad debts.

When you review the management letter, remember that your auditor isn’t grading your performance. The letter is designed to provide advice based on best practices that the audit team has learned over the years from working with other clients.

Observant auditors may comment on a wide range of issues they encounter during the course of an audit. Examples — beyond internal controls — include cash management, operating workflow, control of production schedules, capacity issues, defects and waste, employee benefits, safety, website management, technology improvements and energy consumption.

Take your audit to the next level

Always take the time to review the management letter that’s delivered with your audited financial statements — don’t just file it away for a later date. Too often, the same talking points are repeated year after year. Proactive managers recognize the valuable insights these letters contain, and they contact us to discuss how to implement changes as soon as possible.

© 2022

The April tax filing deadline has passed, but that doesn’t mean you should push your taxes out of your mind until next year. Here are three tax-related actions that you should consider taking in the near term (if you filed on time and didn’t file for an extension).

Retain the requisite records

Depending on the specific issue, the IRS has years to audit your tax return so it’s critical to maintain the records you may need to defend yourself. You generally need to keep the documents that support your income, deductions and credits for at least three years after the tax-filing deadline. (Note that no time limit applies to how long the IRS has to pursue taxpayers who don’t file or file fraudulent returns.)

Essential documentation to retain may include:

- Form W-2, “Wage and Tax Statement,”

- Form 1099-NEC, “Nonemployee Compensation,” 1099-MISC, “Miscellaneous Income,” and 1099-G, “Certain Government Payments,”

- Form 1098, “Mortgage Interest Statement,”

- Property tax payments,

- Charitable donation receipts,

- Records related to contributions to and withdrawals from Section 529 plans and Health Savings Accounts, and

- Records related to deductible retirement plan contributions.

Hold on to records relating to property (including improvements to property) until the period of limitations expires for the year in which you dispose of the property. You’ll need those records to calculate your gain or loss.

Plan for your 2022 taxes

You should be collecting the documentation you’ll need for next year’s tax filing deadline on an ongoing basis. Keep up-to-date records of items such as charitable donations and mileage expenses.

In addition, this is a good time to reassess your current tax withholding to determine if you need to update your Form W-4, “Employee’s Withholding Certificate.” You may want to increase withholding if you owed taxes this year. Conversely, you might want to reduce it if you received a hefty refund. Changes also might be in order if you expect to experience certain major life changes, such as marriage, divorce, childbirth or adoption this year.

If you make estimated tax payments throughout the year, consider reevaluating the amounts you pay. You might want to increase or reduce the payments on account of changes in self-employment income, investment income, Social Security benefits and other types of nonwage income. To preempt the risk of a penalty for underpayment of estimated tax, consider paying at least 90% of the tax for the current year or 100% of the tax shown on your prior year’s tax return, whichever amount is less.

When it comes to strategies to reduce your 2022 tax bill, recent downturns in the stock market may have some upside. If you have substantial funds in a traditional IRA, this could be a ripe time to convert them to a Roth IRA. Roth IRAs have no required mandatory distributions, and distributions are tax-free. You must pay income tax on the fair market value of the converted assets, but, if you convert securities that have fallen in value or you’re in a lower tax bracket in 2022, you could pay less in taxes now than you would in the future. Moreover, any subsequent appreciation will be tax-free.

The market downturn could provide loss-harvesting opportunities, too. By selling poorly performing investments before year end, you can offset realized taxable gains on a dollar-for-dollar basis. If you end up with excess losses, you generally can apply up to $3,000 against your ordinary income and carry forward the balance to future tax years.

If you itemize deductions on your tax return, you also might consider “bunching” expected medical expenses into 2022 to increase the odds that you can claim the medical and dental expense deduction. You’re allowed to deduct unreimbursed expenses that exceed 7.5% of your adjusted gross income. If you expect to have, for example, a knee replacement surgery next winter, accelerating it (and all of the follow-up appointments and physical therapy) into this year could put you over the 7.5% threshold.

Respond to an IRS question or audit

You might have no choice but to continue thinking about your taxes if you receive a tax return question or audit letter from the IRS (and you would be notified only by a letter — the IRS doesn’t initiate inquiries or audits by telephone, text or email). Such letters can be alarming, but don’t assume the worst.

It’s important to remember that receiving a question or being selected for an audit doesn’t always mean you’ve tripped up somehow. For example, your tax return could have been flagged based on a statistical formula that compares similar returns for deviations from “norms.”

Further, if selected, you’re most likely going to undergo a correspondence audit; these audits account for more than 70% of IRS audits. They’re conducted by mail for a single tax year and involve only a few issues that the IRS anticipates it can resolve by reviewing relevant documents. According to the IRS, most audits involve returns filed within the last two years.

If you receive notification of a correspondence audit, you and your tax advisor should closely follow the instructions. You can request additional time if you can’t submit all documentation requested by the specified deadline. It’s advisable to submit copies instead of original documents, and each page of documentation should be marked with your name, Social Security number and the tax year under scrutiny.

Don’t ignore the letter. Doing so will eventually lead to the IRS disallowing the item(s) claimed and issuing a Notice of Deficiency (that is, a notice that a balance is due). You’ll then have 90 days to petition the U.S. Tax Court for review.

While correspondence audits are by far the most common, you could be selected for an office audit (in an IRS office) or field audit (at the taxpayer’s place of business). These are more intensive, and you should consult a tax professional with expertise in handling these types of exams.

Stay ahead of the game

Tax planning is an ongoing challenge. We can help you take the necessary steps to minimize your filing burden, your tax liability and the risk of bad results if you’re ever flagged for an audit.

© 2022

If you donate valuable items to charity, you may be required to get an appraisal. The IRS requires donors and charitable organizations to supply certain information to prove their right to deduct charitable contributions. If you donate an item of property (or a group of similar items) worth more than $5,000, certain appraisal requirements apply. You must:

- Get a “qualified appraisal,”

- Receive the qualified appraisal before your tax return is due,

- Attach an “appraisal summary” to the first tax return on which the deduction is claimed,

- Include other information with the return, and

- Maintain certain records.

Keep these definitions in mind. A qualified appraisal is a complex and detailed document. It must be prepared and signed by a qualified appraiser. An appraisal summary is a summary of a qualified appraisal made on Form 8283 and attached to the donor’s return.

While courts have allowed taxpayers some latitude in meeting the “qualified appraisal” rules, you should aim for exact compliance.

The qualified appraisal isn’t submitted separately to the IRS in most cases. Instead, the appraisal summary, which is a separate statement prepared on an IRS form, is attached to the donor’s tax return. However, a copy of the appraisal must be attached for gifts of art valued at $20,000 or more and for all gifts of property valued at more than $500,000, other than inventory, publicly traded stock and intellectual property. If an item has been appraised at $50,000 or more, you can ask the IRS to issue a “Statement of Value” that can be used to substantiate the value.

Failure to comply with the requirements

The penalty for failing to get a qualified appraisal and attach an appraisal summary to the return is denial of the charitable deduction. The deduction may be lost even if the property was valued correctly. There may be relief if the failure was due to reasonable cause.

Exceptions to the requirement

A qualified appraisal isn’t required for contributions of:

- A car, boat or airplane for which the deduction is limited to the charity’s gross sales proceeds,

- stock in trade, inventory or property held primarily for sale to customers in the ordinary course of business,

- publicly traded securities for which market quotations are “readily available,” and

- qualified intellectual property, such as a patent.

Also, only a partially completed appraisal summary must be attached to the tax return for contributions of:

- Nonpublicly traded stock for which the claimed deduction is greater than $5,000 and doesn’t exceed $10,000, and

- Publicly traded securities for which market quotations aren’t “readily available.”

More than one gift

If you make gifts of two or more items during a tax year, even to multiple charitable organizations, the claimed values of all property of the same category or type (such as stamps, paintings, books, stock that isn’t publicly traded, land, jewelry, furniture or toys) are added together in determining whether the $5,000 or $10,000 limits are exceeded.

The bottom line is you must be careful to comply with the appraisal requirements or risk disallowance of your charitable deduction. Contact us if you have any further questions or want to discuss your contribution planning.

© 2022

The coronavirus pandemic has brought about several new funding streams that your organization may have received. If so, you will likely need to give more consideration to audit and compliance requirements than you have given attention to in previous years. Your organization may even be subject to a single audit for the first time, which could be a daunting process to go through if you are unprepared. Following are some special considerations to think about.

- Will you need a single audit? If you expended more than $750,000 of federal funds, you’ll likely need one (however, more on this below). In basic terms, this a more intensive audit that requires additional reporting outside of your basic financial statement audit. The single audit will communicate:

- an opinion as to whether you have complied with all material compliance requirements of your major federal programs,

- any noncompliance that was noted specific to other laws, regulations, and grant agreements,

- any internal control deficiencies over compliance or financial reporting that were noted during the audit, and

- an opinion as to the accuracy of the schedule of federal awards’ expenditures in relation to your financial statements as a whole.

Your auditor will need to perform a great deal of additional testing to complete this reporting and increased effort to prepare will be required on your part. You should make a single audit determination and let your auditor know as soon as possible, so both parties will have enough notice to plan and prepare for the single audit.

- If a single audit is needed, a new statement called the schedule of expenditures of federal awards (SEFA) will be required. Your auditor will need an accurate schedule well in advance of the audit to communicate which grants will be selected as major programs, meaning the grants that the single audit will give the most attention to. If you have never prepared this schedule before, you may wish to reach out to your auditor for guidance.

- Some of the pandemic funding is not subject to a single audit. Ensure you are familiar with which funding is and is not subject to a single audit for proper reporting on the SEFA. This point is crucial because it could be the difference between having or not having a single audit in the first place.

- Provider Relief Funds are unique funding in that although the funds are received (and possibly expended) in one period, they are not reportable until a future period. This can directly affect your schedule of expenditures of federal awards. Additionally, special audit requirements may apply. If you receive any of this funding, you should become familiar with compliance and reporting requirements.

- All expenditures must be reported separately, by grant, in your general ledger. For example, if you have Federal Grant A and Federal Grant B, you will need a way to associate how much of all costs, such as salaries, are charged to each grant. This is ideally accomplished with separate accounts or separate grant codes within the accounting system. The separation is essential to demonstrate you are not charging the same expenditures to multiple grants or ‘double-dipping.’

- Regardless of whether you need a single audit or not, as a recipient of federal funding, you should have a written procedures manual in addition to your policies that are specific to federal grants. It is important to understand that policies and procedures are two very different things. Your procedures manual should cover all compliance areas applicable to your grants, such as allowable costs and activities, reporting, earmarking, etc. The manual should be specific to your organization and in sufficient detail to document and demonstrate proper procedures, in addition to guiding employees responsible for compliance. The manual is especially important in the event of a changeover in the CFO or compliance officer position.

Ensure you are familiar with both the specific requirements of your grant and the Uniform Guidance (UG), which is outlined in the Code of Federal Regulations at 2 CFR 200. UG is the streamlined and consolidated guidance that governs all federal awards issued on or after December 26, 2014. A great deal of the single audit is focused on compliance with UG.

Contact Yeo & Yeo’s Nonprofit Services Group or your auditor if you think you may need a single audit for the first time or if you need help with any of the special considerations above.

The IRS has begun mailing notices to businesses, financial institutions and other payers that filed certain returns with information that doesn’t match the agency’s records.

These CP2100 and CP2100A notices are sent by the IRS twice a year to payers who filed information returns that are missing a Taxpayer Identification Number (TIN), have an incorrect name or have a combination of both.

Each notice has a list of persons who received payments from the business with identified TIN issues.

If you receive one of these notices, you need to compare the accounts listed on the notice with your records and correct or update your records, if necessary. This can also include correcting backup withholding on payments made to payees.

Which returns are involved?

Businesses, financial institutions and other payers are required to file with the IRS various information returns reporting certain payments they make to independent contractors, customers and others. These information returns include:

- Form 1099-B, Proceeds from Broker and Barter Exchange Transactions,

- Form 1099-DIV, Dividends and Distributions,

- Form 1099-INT, Interest Income,

- Form 1099-K, Payment Card and Third-Party Network Transactions,

- Form 1099-MISC, Miscellaneous Income,

- Form 1099-NEC, Nonemployee Compensation, and

- Form W-2G, Certain Gambling Winnings.

Do you have backup withholding responsibilities?

The CP2100 and CP2100A notices also inform recipients that they’re responsible for backup withholding. Payments reported on the information returns listed above are subject to backup withholding if:

- The payer doesn’t have the payee’s TIN when making payments that are required to be reported.

- The individual receiving payments doesn’t certify his or her TIN as required.

- The IRS notifies the payer that the individual receiving payments furnished an incorrect TIN.

- The IRS notifies the payer that the individual receiving payments didn’t report all interest and dividends on his or her tax return.

Do you have to report payments to independent contractors?

By January first of the following year, payers must complete Form 1099-NEC, “Nonemployee Compensation,” to report certain payments made to recipients. If the following four conditions are met, you must generally report payments as nonemployee compensation:

- You made a payment to someone who isn’t your employee,

- You made a payment for services in the course of your trade or business,

- You made a payment to an individual, partnership, estate, or, in some cases, a corporation, and

- You made payments to a recipient of at least $600 during the year.

Contact us if you receive a CP2100 or CP2100A notice from the IRS or if you have questions about filing Form 1099-NEC. We can help you stay in compliance with all rules.

© 2022

Financial statements tell only part of the story. Investors, lenders and other stakeholders who know how to identify red flags of impending problems can protect their own financial interests. Additional due diligence may be needed to uncover these issues. For instance, stakeholders might need to talk to management, visit the company’s website and compute financial benchmarks using the company’s most recent financial statement. Here’s what to look for.

Employees who jump ship

Employee turnover — at all levels — often precedes weak financial results. One obvious reason is that company insiders are often the first to know when trouble is brewing. For example, if the plant manager’s innovative ideas are frequently denied due to lack of funds or if employees hear shareholders bickering over the company’s strategic direction, they may decide to seek greener pastures.

The reverse happens, too. If certain key people leave the company, it may cause revenue or productivity to nosedive. Given time and sufficient effort, most established companies can recover from the loss of a key person.

Another reason for high employee turnover may be layoffs. Companies that can’t meet payroll may need to shed costs and dole out pink slips.

Employee turnover can also be a vicious cycle. Top performers in an organization may respond to perceived financial problems by moving to healthier competitors. That leaves behind the weaker performers, who must train new hires on the company’s operations. Finding and training new workers can be time-consuming and costly, compounding the borrower’s financial distress.

Working capital concerns

Working capital is the difference between a company’s current assets and liabilities. Monitoring key turnover ratios can help gauge whether the company is managing its short-term assets and liabilities efficiently.

When accounts receivable turnover slows dramatically, it could signal weakened collection efforts, stale accounts or even fraud. For example, a company that’s desperate to boost revenue might solicit business with customers that have poor credit. Or one of a company’s major customers might be underperforming and it’s trickling down the supply chain.

Likewise, beware of deteriorating inventory turnover. Similar to receivables, a buildup of inventory on a borrower’s balance sheet could signal inefficient asset management. Certain product lines may be obsolete and require inventory write-offs. Or a new plant manager might overestimate the amount of buffer stock that’s needed in the warehouse. It might even forewarn of fraud or financial misstatement.

Changing market conditions

External factors may affect a company’s financial performance, but the effects vary from company to company. For instance, some companies permanently closed when the economy shut down during the COVID-19 pandemic, while others pivoted and prospered.

Today, business performance may be adversely impacted by geopolitical pressures, rising interest rates, supply chain shortages and inflation. Stakeholders should continue to monitor financial results closely in these volatile conditions.

Extra assurance

When a company shows signs of financial distress, stakeholders should encourage management to supplement its year-end financial statements with interim reports or engage a CPA to perform targeted agreed-upon procedures. Doing so can help the company assess risk, identify problems and brainstorm corrective measures, if needed. Contact us for more information.

© 2022

Like many people, you may have dreamed of turning a hobby into a regular business. You won’t have any tax headaches if your new business is profitable. But what if the new enterprise consistently generates losses (your deductions exceed income) and you claim them on your tax return? You can generally deduct losses for expenses incurred in a bona fide business. However, the IRS may step in and say the venture is a hobby — an activity not engaged in for profit — rather than a business. Then you’ll be unable to deduct losses.

By contrast, if the new enterprise isn’t affected by the hobby loss rules because it’s profitable, all otherwise allowable expenses are deductible on Schedule C, even if they exceed income from the enterprise.

Note: Before 2018, deductible hobby expenses had to be claimed as miscellaneous itemized deductions subject to a 2%-of-AGI “floor.” However, because miscellaneous deductions aren’t allowed from 2018 through 2025, deductible hobby expenses are effectively wiped out from 2018 through 2025.

Avoiding a hobby designation

There are two ways to avoid the hobby loss rules:

- Show a profit in at least three out of five consecutive years (two out of seven years for breeding, training, showing or racing horses).

- Run the venture in such a way as to show that you intend to turn it into a profit-maker, rather than operate it as a mere hobby. The IRS regs themselves say that the hobby loss rules won’t apply if the facts and circumstances show that you have a profit-making objective.

How can you prove you have a profit-making objective? You should run the venture in a businesslike manner. The IRS and the courts will look at the following factors:

- How you run the activity,

- Your expertise in the area (and your advisors’ expertise),

- The time and effort you expend in the enterprise,

- Whether there’s an expectation that the assets used in the activity will rise in value,

- Your success in carrying on other activities,

- Your history of income or loss in the activity,

- The amount of any occasional profits earned,

- Your financial status, and

- Whether the activity involves elements of personal pleasure or recreation.

Recent court case

In one U.S. Tax Court case, a married couple’s miniature donkey breeding activity was found to be conducted with a profit motive. The IRS had earlier determined it was a hobby and the couple was liable for taxes and penalties for the two tax years in which they claimed losses of more than $130,000. However, the court found the couple had a business plan, kept separate records and conducted the activity in a businesslike manner. The court stated they were “engaged in the breeding activity with an actual and honest objective of making a profit.” (TC Memo 2021-140)

Contact us for more details on whether a venture of yours may be affected by the hobby loss rules, and what you should do to avoid a tax challenge.

© 2022

What are the tax consequences of selling property used in your trade or business?

There are many rules that can potentially apply to the sale of business property. Thus, to simplify discussion, let’s assume that the property you want to sell is land or depreciable property used in your business, and has been held by you for more than a year. (There are different rules for property held primarily for sale to customers in the ordinary course of business; intellectual property; low-income housing; property that involves farming or livestock; and other types of property.)

General rules

Under the Internal Revenue Code, your gains and losses from sales of business property are netted against each other. The net gain or loss qualifies for tax treatment as follows:

1) If the netting of gains and losses results in a net gain, then long-term capital gain treatment results, subject to “recapture” rules discussed below. Long-term capital gain treatment is generally more favorable than ordinary income treatment.

2) If the netting of gains and losses results in a net loss, that loss is fully deductible against ordinary income (in other words, none of the rules that limit the deductibility of capital losses apply).

Recapture rules

The availability of long-term capital gain treatment for business property net gain is limited by “recapture” rules — that is, rules under which amounts are treated as ordinary income rather than capital gain because of previous ordinary loss or deduction treatment for these amounts.

There’s a special recapture rule that applies only to business property. Under this rule, to the extent you’ve had a business property net loss within the previous five years, any business property net gain is treated as ordinary income instead of as long-term capital gain.

Section 1245 Property

“Section 1245 Property” consists of all depreciable personal property, whether tangible or intangible, and certain depreciable real property (usually, real property that performs specific functions). If you sell Section 1245 Property, you must recapture your gain as ordinary income to the extent of your earlier depreciation deductions on the asset.

Section 1250 Property

“Section 1250 Property” consists, generally, of buildings and their structural components. If you sell Section 1250 Property that was placed in service after 1986, none of the long-term capital gain attributable to depreciation deductions will be subject to depreciation recapture. However, for most noncorporate taxpayers, the gain attributable to depreciation deductions, to the extent it doesn’t exceed business property net gain, will (as reduced by the business property recapture rule above) be taxed at a rate of no more than 28.8% (25% as adjusted for the 3.8% net investment income tax) rather than the maximum 23.8% rate (20% as adjusted for the 3.8% net investment income tax) that generally applies to long-term capital gains of noncorporate taxpayers.

Other rules may apply to Section 1250 Property, depending on when it was placed in service.

As you can see, even with the simplifying assumptions in this article, the tax treatment of the sale of business assets can be complex. Contact us if you’d like to determine the tax consequences of specific transactions or if you have any additional questions.

© 2022

AmazonSmile is an accessible, no-cost fundraising opportunity operated by Amazon.com that can help supplement the existing charitable contributions a nonprofit organization receives. The process is simple and it all starts with Amazon.com customers. Customers interested in participating are required to select a charitable organization before making purchases. The AmazonSmile Foundation will then donate 0.5 percent of eligible purchases to the charitable organization of the customer’s choosing. AmazonSmile provides a database of almost one million charitable organizations from GuideStar.com, so your organization may already be able to participate!

Your charitable organization only needs to do two things to maximize the benefit from AmazonSmile.

1. Register to ensure your charitable organization’s information is accurate and to receive the donations that AmazonSmile collected.

2. Make your volunteers and contributors aware of the AmazonSmile program through social marketing or other advertising so they can associate your charitable organization with any Amazon.com purchases they make. There is no cost to the customer nor to the charitable organization for using the service, which makes it a very economical way to embrace existing donors into further supporting your organization.

Go to org.amazon.com for more information and to register. If you have questions, please contact your Yeo & Yeo Non-Profit professional.

Yeo & Yeo CPAs & Business Consultants is pleased to announce that Megan LaPointe, CPP, Lead Payroll Specialist, has met the requirements of the Certification Board of the American Payroll Association and earned the Certified Payroll Professional (CPP) accreditation. A CPP is a specialist in payroll processing and administration.

“The CPP credential is considered the mark of excellence for payroll professionals,” said Christine Porras, CPP, Payroll Services Group leader. “Megan’s achievement demonstrates our professionals’ commitment to expanding Yeo & Yeo’s level of expertise in providing outsourced payroll and consulting services for Michigan businesses.”

All CPPs must pass a rigorous exam and demonstrate knowledge of core payroll concepts, the Fair Labor Standards Act, employment taxes, compensation and benefits, employee and employer forms, voluntary and involuntary deductions, methods and timing of pay, reporting, compliance, internal controls and accounting principles.

Megan LaPointe, a graduate of Northwood University, holds a bachelor’s degree in accounting. She joined Yeo & Yeo in 2015, and is the Lead Payroll Specialist, based in the firm’s Saginaw office. Her areas of expertise include processing payroll, preparing quarterly and annual payroll returns, and payroll audits. Megan is a member of the American Payroll Association – Great Lakes Bay Chapter.

Is your business ready to seek funding from outside investors? Perhaps you’re a start-up that needs money to launch as robustly as possible. Or maybe your company has been operating for a while and you want to pivot in a new direction or just take it to the next level.

Whatever the case may be, seeking outside investment isn’t as cut and dried as applying for a commercial loan. You need to wow investors with your vision, financials and business plan.

To do so, many businesses today put together a “pitch deck.” This is a digital presentation that provides a succinct, compelling description of the company, its solution to a market need, and the benefits of the investment opportunity. Here are some useful guidelines:

Keep it brief, between 10 to 12 short slides. You want to make a positive impression and whet investors’ interest without taking up too much of their time. You can follow up with additional details later.

Be concise but comprehensive. State your company’s mission (why it exists), vision (where it wants to go) and value proposition (what your product or service does for customers). Also declare upfront how much money you’d like to raise.

Identify the problem you’re solving. Explain the gap in the market that you’re addressing. Discuss it realistically and with minimal jargon, so investors can quickly grasp the challenge and intuitively agree with you.

Describe your target market. Include the market’s size, composition and forecasted growth. Resist the temptation to define the market as “everyone,” because this tends to come across as unrealistic.

Outline your business plan. That is, how will your business make money? What will you charge customers for your solution? Are you a premium provider or is this a budget-minded product or service?

Summarize your marketing and sales plans. Describe the marketing tactics you’ll employ to garner attention and interact with your customer base. Then identify your optimal sales channels and methods. If you already have a strong social media following, note that as well.

Sell your leadership team. Who are you and your fellow owners/executives? What are your educational and business backgrounds? Perhaps above everything else, investors will demand that a trustworthy crew is steering the ship.

Provide a snapshot of your financials, both past and future. But don’t just copy and paste your financial statements onto a few slides. Use aesthetically pleasing charts, graphs and other visuals to show historical results (if available), as well as forecasted sales and income for the next several years. Your profit projections should realistically flow from historical performance or at least appear feasible given expected economic and market conditions.

Identify your competitors. What other companies are addressing the problem that your product or service solves? Differentiate yourself from those businesses and explain why customers will choose your solution over theirs.

Describe how you’ll use the funds. Show investors how their investment will allow you to fulfill your stated business objectives. Be as specific as possible about where the money will go.

Ask for help. As you undertake the steps above — and before you meet with investors — contact our firm. We can help you develop a pitch deck with accurate, pertinent financial data that will capture investors’ interest and help you get the funding your business needs.

© 2022

Adding a new partner in a partnership has several financial and legal implications. Let’s say you and your partners are planning to admit a new partner. The new partner will acquire a one-third interest in the partnership by making a cash contribution to it. Let’s further assume that your bases in your partnership interests are sufficient so that the decrease in your portions of the partnership’s liabilities because of the new partner’s entry won’t reduce your bases to zero.

Not as simple as it seems

Although the entry of a new partner appears to be a simple matter, it’s necessary to plan the new person’s entry properly in order to avoid various tax problems. Here are two issues to consider:

First, if there’s a change in the partners’ interests in unrealized receivables and substantially appreciated inventory items, the change is treated as a sale of those items, with the result that the current partners will recognize gain. For this purpose, unrealized receivables include not only accounts receivable, but also depreciation recapture and certain other ordinary income items. In order to avoid gain recognition on those items, it’s necessary that they be allocated to the current partners even after the entry of the new partner.

Second, the tax code requires that the “built-in gain or loss” on assets that were held by the partnership before the new partner was admitted be allocated to the current partners and not to the entering partner. Generally speaking, “built-in gain or loss” is the difference between the fair market value and basis of the partnership property at the time the new partner is admitted.

The most important effect of these rules is that the new partner must be allocated a portion of the depreciation equal to his share of the depreciable property based on current fair market value. This will reduce the amount of depreciation that can be taken by the current partners. The other effect is that the built-in gain or loss on the partnership assets must be allocated to the current partners when partnership assets are sold. The rules that apply here are complex and the partnership may have to adopt special accounting procedures to cope with the relevant requirements.

Keep track of your basis

When adding a partner or making other changes, a partner’s basis in his or her interest can undergo frequent adjustment. It’s imperative to keep proper track of your basis because it can have an impact in several areas: gain or loss on the sale of your interest, how partnership distributions to you are taxed and the maximum amount of partnership loss you can deduct.

Contact us if you’d like help in dealing with these issues or any other issues that may arise in connection with your partnership.

© 2022

In today’s volatile economy, many businesses and nonprofits have been required to write down the value of acquired goodwill on their balance sheets. Others are expected to follow suit — or report additional write-offs — in 2022. To the extent that goodwill is written off, it can’t be recovered in the future, even if the organization recovers. So, impairment testing is a serious endeavor that usually requires input from your CPA to ensure accuracy, transparency and timeliness.

Reporting goodwill

Under U.S. Generally Accepted Accounting Principles (GAAP), when an organization merges with or acquires another entity, the acquirer must allocate the purchase price among the assets acquired and liabilities assumed, based on their fair values. If the purchase price is higher than the combined fair value of the acquired entity’s identifiable net assets, the excess value is labeled as goodwill.

Before lumping excess value into goodwill, acquirers must identify and value other identifiable intangible assets, such as trademarks, customer lists, copyrights, leases, patents or franchise agreements. An intangible asset is recognized apart from goodwill if it arises from contractual or legal rights — or if it can be sold, transferred, licensed, rented or exchanged.

Goodwill is allocated among the reporting units (or operating segments) that it benefits. Many small private entities consist of a single reporting unit. But large conglomerates may be composed of numerous reporting units.

Testing for impairment

Organizations must generally test goodwill and other indefinite-lived intangibles for impairment each year. More frequent impairment tests might be necessary if other triggering events happen during the year — such as the loss of a key person, unanticipated competition, reorganization or adverse regulatory actions.

In lieu of annual impairment testing, private entities have the option to amortize acquired goodwill over a useful life of up to 10 years. In addition, the Financial Accounting Standards Board recently issued updated guidance that allows private companies and not-for-profits to delay the assessment of the goodwill impairment triggering event until the first reporting date after that triggering event. The change aims to reduce costs and simplify impairment testing related to triggering events.

Writing down goodwill

When impairment occurs, the organization must decrease the carrying value of goodwill on the balance sheet and reduce its earnings by the same amount. Impairment charges are a separate line item on the income statement that may have real-world consequences.

For example, some organizations reporting impairment losses may be in technical default on their loans. This situation might require management to renegotiate loan terms or find a new lender. Impairment charges also raise a red flag to investors and other stakeholders.

Who can help?

Few organizations employ internal accounting staff with the requisite training to measure impairment. Contact us for help navigating this issue and its effects on your financial statements.

© 2022