To prevent and detect vendor fraud, first we need to understand what fraud is and why it occurs.

Fraud is a deception that is intentional and caused by an employee or organization for personal gain. In other words, fraud is a deceitful activity used to gain an advantage or generate an illegal profit. Also, the unlawful act benefits the perpetrator and harms other parties involved, such as your school district.

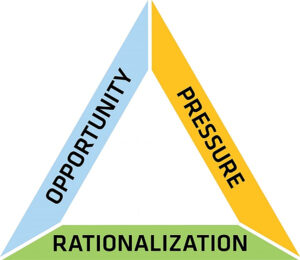

Understanding the fraud triangle provides excellent insight as to why fraud occurs. The fraud triangle is a framework for spotting high-risk fraud situations. The three parts of the fraud triangle are Pressure/Incentive, Opportunity, and Rationalization.

- Pressure/Incentive – Financial hardships, personality changes, living beyond one’s means, outside business interests, unwillingness to share workplace duties, and need to meet budgets/projections.

- Opportunity – Weak internal controls, poor oversight, poor tone at the top, and inadequate accounting policies and procedures.

- Rationalization – I’m underpaid! The boss steals; why not me? It’s just a loan! I volunteer – I deserve something! I am working more and getting paid less! Whatever a person can tell themselves to make it seem okay.

In the fraud triangle, school districts have the most control over opportunity. You can’t control a person’s rationalization or the outside pressures on them; however, you can put controls in place in your district to prevent fraud from occurring.

Common purchasing/vendor frauds that happen at school districts include:

- Fictitious vendors set up by employees

- Use of foodservice supplies for personal catering business

- Purchasing construction supplies for private residence from bond money

- Falsification of records by vendors

- Personal utility bills paid with school district funds

- Approving invoices to pay for goods/services not received

- Bid rigging for a specific vendor

- Collusion with or kickback from a vendor

When it comes to preventing fraud, the best defense is a good offense:

- Solid internal controls that are implemented and followed correctly are the best deterrent to fraud.

- Policies and procedures should be designed to provide reasonable assurance that the school district’s assets are safeguarded against unauthorized use and disposition.

- Internal controls must include segregation of duties, examining supporting documentation before making payment, reconciling bank statements promptly, and safeguarding the school district’s assets.

Segregation of duties is designed to cross-reference each other for accuracy. Giving a single person unquestioned authority over finances is not a wise business practice. Checks and balances help to eliminate the opportunity for fraud and abuse.

Additional prevention and detection techniques include:

- Know your district’s policies and procedures well and make them available and accessible to all employees at the school district.

- Set a strong tone from the top. This is a potent and cheap deterrent to implement. Communicate a policy of zero-tolerance through words and actions. Communicate to employees what constitutes fraud and how it impacts the district. If employees see upper-level management misconduct, they think it is okay for them.

- Establish a vendor code of conduct policy. Place limits on gifts to the school district. Require disclosure of any personal relationships. Ask vendors to sign annually.

- Know your vendor listing and keep it current. Be mindful of new vendors and long-term vendors. Disable all unused vendors.

- Perform walk-throughs of your procurement/payment system from the purchase requisition all the way to receipt of goods and payment to the vendor.

- Randomly select transactions throughout the year and verify all documentation and approvals for purchases are present. Mix up the selections from bids to small purchases and even recurring vendors.

- Implement a fraud hotline/website. Give your employees an outlet to communicate confidentially and reinforce an open-door policy.

- Think like an auditor – be skeptical of transactions! Perform unplanned internal audits on invoice support. Perform research on new vendors. Perform data analysis on your vendor listing.

If you have questions regarding fraud, how to strengthen internal controls, or internal audit procedures you can perform to prevent and detect vendor fraud, please contact your local Yeo & Yeo school district auditor.