Nonprofit Quick Tip: Understand the Fraud Triangle

The fraud triangle was introduced by Donald Cressey in the 1970s. Those who lead nonprofit organizations should understand this model for explaining the factors that cause someone to commit fraud – it’s still relevant today.

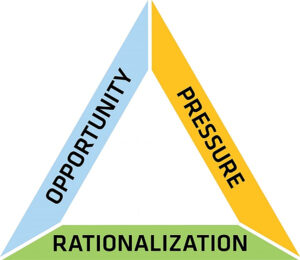

An individual must feel pressure, something that makes them feel a financial burden that they can’t share. For example, this could be unexpected medical bills or a gambling problem. The individual must recognize an opportunity to use their position to ease their financial pressure and not get caught. Nobody else is looking or double-checking, and they have access to the organization’s assets. Most people don’t think of themselves as bad people, so they find ways to rationalize or justify their actions. They might tell themselves, “I’m just borrowing it; I’ll pay it back,” or “I work so hard for this organization, they owe me.

Organizations don’t have control over the pressure an employee is facing or whether or not the employee can rationalize their decisions. However, they can reduce the opportunity that employee has by implementing appropriate internal controls.

Contact Yeo & Yeo for help with implementing fraud prevention and detection measures in your nonprofit organization.

The Fraud Triangle