Michigan Farmland and Forest Preservation Programs Offer Tax Benefits

The State of Michigan has developed several programs that aim to protect and control the use of farmland and forest property. They seek to safeguard open area lands from being turned into commercial or industrial property. This article will outline three programs: The Farmland and Open Space Preservation Program (formerly PA-116), the Conservation Easement Donation Program, and the Qualified Forest Program.

Farmland and Open Space Preservation Program

The Farmland and Open Space Preservation Program is designed to preserve farmland and open areas from becoming developed into space for commercial or industrial use. To enter into an agreement, the landowner must agree to keep the selected parcel(s) as agricultural land for a minimum of ten years. After the initial agreement expires, the landowner can extend the agreement for a minimum of seven years for as long as the agreement is intended, for agricultural use. Land must be at least 51% devoted to agricultural use to qualify for the credit, and the State of Michigan just passed a bill in March that allows landowners to carve out sections of a parcel that are not used for agricultural purposes (i.e., a house on a parcel that includes farmland). The largest benefit for a landowner is the credit they are eligible for on their Michigan income tax return. All property taxes (less special assessments) paid over 3.5% of household income are deemed a dollar-for-dollar reduction of tax owed, with all excess refunded to the taxpayer.

Conservation Easement Program

The Conservation Easement Program is a tool used by the State of Michigan and a private landowner to prohibit the development of farmland. These agreements are enforced to protect the agricultural value of the property. A conservation easement donation is an approach to keep land permanently protected, while the landowner still controls the parcel. The largest benefit of this program to a landowner who enters into an agreement is the possibility that the land donation could qualify as a charitable donation that could be deducted on a federal income tax return. Property taxes could also be lowered based on the new assessed value of the land.

Qualified Forest Program

Michigan is home to more than 20 million acres of forestland, and the State has developed a program that makes it beneficial for landowners to keep their forest undeveloped. To qualify for the benefit, parcels of land between 20 and 39 acres must be more than 80% populated with forest capable of being produced into wood products, and parcels larger than 40 acres need to be at least 50% capable of producing wood product. The largest tax benefit from entering into an agreement would be the reduction of the school operating fund taxes on non-homestead property tax statements. The reduction is a maximum of 18 mills; the school operating fund accounts for the largest single item on a property tax bill.

Using these programs can prove to be advantageous for many taxpayers, and can be a very useful tax planning tool. If you believe that you may have a parcel of land that qualifies for any of the above programs, please contact Yeo & Yeo for more information or help to get the process started.

Often clients ask me, “How can I move income into next year?” I tell them that if they correctly calculate their work in process, it will reduce the amount of income recognized for the year.

When materials are purchased for jobs, construction companies often include all the inventory purchased in the percentage completed immediately, rather than when it is installed on the job. Ultimately this increases the amount of income recognized on these jobs at the end of the first year and decreases income when the job is completed. Start by asking yourself, are the materials located at a job site contributing toward the completion of a specific job? Or, are the materials purchased simply general materials and supplies that are usable for any number of jobs?

If the materials have not been installed and are not unique to a specific job, then they should be classified as inventory. Why inventory? If you have a spool of uninstalled wiring located at a job site that you could take and use on another job, it is not contributing to the completion of that job even though it is located at the job site. Construction companies can, and often do, have inventory located at multiple job sites that is not specific to any one job, which should not be assigned to a job until it is installed.

A simple indicator of projects that may be in need of an adjustment are jobs with a high material to labor ratio. If a company has a job with high material costs and low labor costs, material costs could be contributing a higher percentage completed than is actually completed. Of course, there are always exceptions such as custom-built items for a specific project that cannot be used at another job site.

By properly tracking which materials should be inventory and which materials have been used on the job, you can accurately recognize the profit and pay taxes on the work that is completed instead of work that has not been performed. After all, most of us would rather pay taxes later rather than today.

At the recent Michigan School Business Officials conference, Jennifer Watkins of Yeo & Yeo CPAs and Gloria Suggitt, Michigan Department of Education Single Audit Grant Coordinator, presented, “I Love a Good Audit.” The presentation focused on updates to the Audit Manual and other common issues that the Michigan Department of Education (MDE) will notice and ask districts to correct, change and explain. The presentation also looked at common issues from the auditors’ side, revealing what auditors look for and how to ensure districts do not receive a finding or a letter from the MDE.

The presentation covered timing and responsibility for audit submission, issues with recording commodities, requirements of a corrective action plan, requirements for subrecipient schedules per the MDE and how that format differs from Uniform Guidance, and Uniform Budget and Accounting Act tolerance levels for the MDE versus auditors.

At the end of the presentation, Jennifer spoke on new guidance issued by the state for GASB 68 and provided a list of what the district should have ready for GASB 68 during the audit. The audience enjoyed the presentation and getting an “insider’s” look into the audit. Now they have the edge over others and should have a clean, smooth audit season.

See Jennifer and Gloria’s presentation, I Love a Good Audit.

At the recent Michigan School Business Officials conference, Jennifer Watkins presented, “The ABCs of Your Single Audit.” She spoke about how to prepare the Schedule of Expenditures of Federal Awards (SEFA), SEFA reconciliation and notes, and other necessary schedules. She also shared information on hot topics such as Uniform Grant Guidance and final guidance from the Michigan Department of Education including the current Audit Manual and common issues to watch for in audits and monitoring.

Specifically, Jennifer focused on issues related to time and effort, lack of federal procedures, unallowable costs, improper budgeting, equipment reporting, and policies and requirements that are mandatory for the School Food Authority (nutrition/lunch program).

See her presentation, The ABCs of Your Single Audit.

Operating a business provides a tax benefit if you have an unprofitable year: You can use the loss to offset other income. But you can lose that tax benefit if the IRS views your business as a hobby. Private companies with more than one owner should have a buy-sell agreement to spell out how ownership shares will change hands should an owner depart. For businesses structured as C corporations, the agreements also have significant tax implications that are important to understand.

Buy-sell basics

A buy-sell agreement sets up parameters for the transfer of ownership interests following stated “triggering events,” such as an owner’s death or long-term disability, loss of license or other legal incapacitation, retirement, bankruptcy, or divorce. The agreement typically will also specify how the purchase price for the departing owner’s shares will be determined, such as by stating the valuation method to be used.

Another key issue a buy-sell agreement addresses is funding. In many cases, business owners don’t have the cash readily available to buy out a departing owner. So insurance is commonly used to fund these agreements. And this is where different types of agreements — which can lead to tax issues for C corporations — come into play.

Under a cross-purchase agreement, each owner buys life or disability insurance (or both) that covers the other owners, and the owners use the proceeds to purchase the departing owner’s shares. Under a redemption agreement, the company buys the insurance and, when an owner exits the business, buys his or her shares.

Sometimes a hybrid agreement is used that combines aspects of both approaches. It may stipulate that the company gets the first opportunity to redeem ownership shares and that, if the company is unable to buy the shares, the remaining owners are then responsible for doing so. Alternatively, the owners may have the first opportunity to buy the shares.

C corp. tax consequences

A C corp. with a redemption agreement funded by life insurance can face adverse tax consequences. First, receipt of insurance proceeds could trigger corporate alternative minimum tax.

Second, the value of the remaining owners’ shares will probably rise without increasing their basis. This, in turn, could drive up their tax liability if they later sell their shares.

Heightened liability for the corporate alternative minimum tax is generally unavoidable under these circumstances. But you may be able to manage the second problem by revising your buy-sell as a cross-purchase agreement. Under this approach, owners will buy additional shares themselves — increasing their basis.

Naturally, there are downsides. If owners are required to buy a departing owner’s shares, but the company redeems the shares instead, the IRS may characterize the purchase as a taxable dividend. Your business may be able to mitigate this risk by crafting a hybrid agreement that names the corporation as a party to the transaction and allows the remaining owners to buy back the shares without requiring them to do so.

For more information on the tax ramifications of buy-sell agreements, contact us. And if your business doesn’t have a buy-sell in place yet, we can help you figure out which type of funding method will best meet your needs while minimizing any negative tax consequences.

© 2017

GASB 74 and 75 will have a significant impact on the governmental sector’s financial statements as amounts related to other post-employment benefits are recorded. Make sure you are prepared for a successful implementation by understanding how the financial statements will be altered and what conversations you should have as you prepare for and implement these standards.

See, OPEB Reporting: Embracing GASB 74 and 75 for detailed information.

The White House released the “core principles” of President Trump’s tax plan on Wednesday, April 26, led in a press briefing by Treasury Secretary Steven Mnuchin and National Economic Council director Gary Cohn.

Secretary Mnuchin stated the “core principles” would be worked on with Congress to produce a bill that can be passed. In answer to questions, he said the plan “would pay for itself through economic growth, and by reducing tax deductions and closing loopholes.”

Director Cohn and Secretary Mnuchin stated throughout the briefing that many details were still to be negotiated. Trump’s new tax plan could vastly reduce the amount paid by corporations and individuals across the U.S.; however, crucial details of the new plan remain unknown. Here is what we do know:

Tax reform goals:

- Grow the economy and create millions of jobs

- Simplify our burdensome tax code

- Provide tax relief to American families—especially middle-income families

- Lower the business tax rate from one of the highest in the world to one of the lowest

For business taxpayers:

- The business tax rate would decrease from 35% to 15% for corporations, and the top tax rate for pass-through businesses (e.g., partnerships, sole proprietorships) would be reduced from 39.6% to 15%.

- There would be a one-time repatriation tax on offshore earnings. The exact percentage of the tax rate is still being negotiated; previous reports indicated 10% was being considered.

- There would be a shift from a worldwide system of taxation (under which a U.S. taxpayer is taxed on its worldwide income regardless of where it was earned) to a territorial system (under which income would be taxed in the country where it is earned).

For individual taxpayers:

Tax relief to American families—especially middle-income families:

- The current seven income tax brackets would be reduced to three: 10%, 25% and 35%. The levels at which these brackets would apply have not yet been determined.

- The standard deduction would be doubled, with the intended result being that fewer taxpayers would itemize.

Simplification:

- Eliminate tax deductions that “mainly benefit the wealthiest taxpayers” other than the mortgage interest and charitable contribution deductions. Interestingly, state and local taxes would no longer be deductible.

- Repeal the alternative minimum tax.

- Repeal the estate tax.

- Repeal the 3.8% net investment income tax (which was enacted as part of the Affordable Care Act).

It is stated that during the month of May, the Trump Administration will hold listening sessions with stakeholders to receive their input. The Administration will also continue to work with the House and Senate to develop the details of a plan that provides massive tax relief, creates jobs, and makes America more competitive—and can pass both chambers. No firm deadline was placed on the proceedings.

With many details to iron out, we will need to wait and see what emerges during the legislative process. Yeo & Yeo will keep you informed as new details unfold.

Each year, millions of taxpayers claim an income tax refund. To be sure, receiving a payment from the IRS for a few thousand dollars can be a pleasant influx of cash. But it means you were essentially giving the government an interest-free loan for close to a year, which isn’t the best use of your money.

Fortunately, there is a way to begin collecting your 2017 refund now: You can review the amounts you’re having withheld and/or what estimated tax payments you’re making, and adjust them to keep more money in your pocket during the year.

Reasons to modify amounts

It’s particularly important to check your withholding and/or estimated tax payments if:

- You received an especially large 2016 refund,

- You’ve gotten married or divorced or added a dependent,

- You’ve purchased a home,

- You’ve started or lost a job, or

- Your investment income has changed significantly.

Even if you haven’t encountered any major life changes during the past year, changes in the tax law may affect withholding levels, making it worthwhile to double-check your withholding or estimated tax payments.

Making a change

You can modify your withholding at any time during the year, or even several times within a year. To do so, you simply submit a new Form W-4 to your employer. Changes typically will go into effect several weeks after the new Form W-4 is submitted. For estimated tax payments, you can make adjustments each time quarterly payments are due.

While reducing withholdings or estimated tax payments will, indeed, put more money in your pocket now, you also need to be careful that you don’t reduce them too much. If you don’t pay enough tax during the year, you could end up owing interest and penalties when you file your return, even if you pay your outstanding tax liability by the April 2018 deadline.

If you’d like help determining what your withholding or estimated tax payments should be for the rest of the year, please contact us.

© 2017

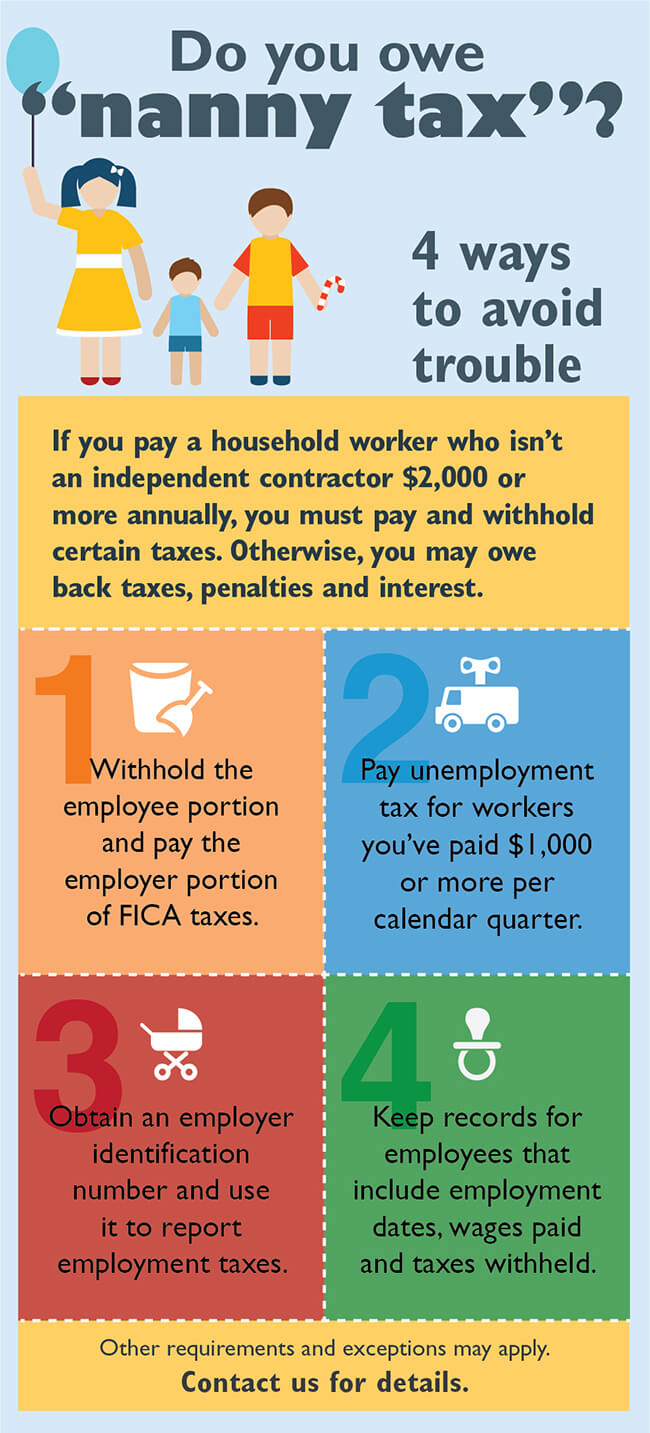

Are you considering hiring someone to regularly help out around the house, either with the kids, caring for another family member or performing chores or errands? Or have you already made some informal arrangements that you’ve been handling on your own, but you’re not quite sure you’re taking care of all the details?

Just because your nanny or other household help is paid in cash or feels like part of the family doesn’t mean that the rules don’t apply.

If you think you may not be in compliance for state or federal tax purposes with your household helpers, stop worrying and let us help manage your filing requirements!

The Michigan School Business Officials Annual Conference will be held at the DeVos Place in Grand Rapids, May 2-4. Members of Yeo & Yeo’s Education Services Group will present four of the sessions. We welcome you to join us to gain new insights into managing your Michigan school.

- Ethics Dilemmas and Fraud & Forensics Prevention – Molly Fish, CPA

Learn about the common ethical dilemmas that arise in school districts and examine examples of actual Fraud & Forensics that has occurred at local school districts. Find out what you can do to prevent it from happening at your district.

- The ABCs of Your District’s Single Audit – Jennifer Watkins, CPA

Learn how to prepare for your single audit, including the Schedule of Expenditures of Federal Awards (SEFA) preparation and common findings. Learn the changing requirements of a single audit.

- Ask the Auditor – David Youngstrom, CPA, and Brian Dixon, CPA

Have an off-the-record discussion with experienced school auditors in a “penalty free” zone. Whether you have been doing this for years or are just starting out, bring your questions or your scenarios to get instant feedback!

- cybersecurity – Kristi Krafft-Bellsky, CPA

Find out how to verify that your information is protected and what you should be asking as a technology director.

We encourage you to attend. Register and learn more about the MSBO Annual Conference.

Nonprofits with years ending December 31, 2018, and later will implement the new nonprofit accounting standard, FASB ASU 2016-14, Presentation of Financial Statements of Non-Profit Entities. This new standard is the first significant change to nonprofit accounting in 20 years. One of the key changes in this standard relates to functional expenses.

Under the current standards, voluntary health and welfare organizations must present a statement of functional expenses that breaks down, in a grid format, natural and functional expense classifications. Also, all nonprofits must report their expenses on a functional basis, which can be done on the face of the statement of activities, in a statement of functional expenses, or in a footnote to the financials. Under the new standard, all nonprofits will be required to provide an analysis of expenses by their nature and function.

For voluntary health and welfare organizations, this will look very similar to the current statement of functional expenses, as a statement is one manner in which the information can be provided. For other organizations, this will be a brand new statement or extensive footnote; we recommend a statement for most organizations. Theoretically, those other organizations should have already had a supporting schedule in their work papers to their financial statements showing how they got from the natural expenses to the functional classifications, but many organizations may have simply taken a percentage estimate in total.

Start planning now

If your organization has not previously done a statement of functional expenses, you need to start planning now for how you will obtain the information to be able to create, essentially, a statement of functional expenses. Consider if this is something that should be done via direct allocation as expenses are recorded, and thus may necessitate a change in your chart of accounts structure, or if it is best done using an indirect allocation during the financial statement preparation process. Either way, changes to the internal control structure may be necessary to track the information to properly allocate these expenses in a grid showing natural and functional expenses.

Investment expenses

However, even for those who previously did a statement of functional expenses, there are a few changes. Previously GAAP allowed the netting of investment expense with investment return. Some organizations did this and others did not. Most of the time those expenses were direct expenditures to third parties for investment fees and management. This new standard removes the option, and external investment expenses, as well as direct internal investment expenses, must be netted with investment income.

Organizations may not have procedures in place to track the direct internal investment expenses or to allocate them using an indirect allocation. These expenses include the direct conduct or direct supervision of the strategic and tactical activities involved in generating investment return. For example, if your executive director is involved in the due diligence process for changing investment firms – or if your investment firm provides quarterly meetings that your Controller attends to learn about the investment strategies and options – the time for those is an investment expense that must be netted against investment revenue. Most entities have just considered that internal investment expense to be management and general.

Do be aware, for entities like community foundations, where investing is part of the programmatic achievements, their accounting will not change and their investment income, because it is programmatic, will remain gross. This will involve changes in internal controls over time tracking and possibly expense documentation. It may also involve a change to the chart of accounts to allow those expenses to be broken out in the trial balance.

Other changes

Traditionally certain things may have been excluded or included in the statement of functional expenses that will need to change under the new standard.

- Gains and losses are specifically excluded from this analysis of expenses by nature and function; by definition they are not expenses.

- Certain special event expenses, if the special event is not major and ongoing, have traditionally been netted against revenues. Although they can continue to be netted against revenues, they will also need to appear in this analysis of expenses by nature and function. Also, they have to be included based on the nature of the expense. For example, if you have a gala event that meets the requirements that the special event expenses can be netted against revenues, under the new standard those expenses will need to be in the analysis of expenses by nature and function, and they will go to line items like salaries, entertainment, rent, food, and not to a single line item like gala event.

- Cost of goods sold also has to be broken out by nature, and not just lumped together as one line. This is another area that likely will require either an expansion of the chart of accounts or more detailed recordkeeping.

Management and general expenses vs. program expenses

FASB also strengthened the example of what is management and general versus what is program. Program expenses include the direct conduct or direct supervision of programmatic purposes; they do not include general overall supervision. For example, the program department director reports to the executive director and keeps the executive director in the know about programs; this is not direct conduct or direct supervision on the executive director’s part. However, the program department director is out on medical leave and during that time the executive director is giving directions and following up to specifically manage the staff in the program department to ensure the program is being accomplished; this is direct supervision and would be allocable to program expenses.

The standard calls out financial reporting for grants as being specifically management and general, too. Although we do not believe the intent of the standard has changed, many organizations had different interpretations of the original standard and will see additional management and general expenses under the new standard.

Organizations should start discussing these changes with management, the board, and funding sources to prepare them for changes in the program service expense percentages.

MAS 90 is a brand that has stood the test of time and has become a standard within the manufacturing industry. Manufacturers have relied on the robust, feature-rich application to manage their business processes, from receiving quotes to producing orders and shipping their products on time.

Did you know that the name of the software is no longer MAS 90? Although many users still refer to the software as MAS 90, it has been upgraded and is now called sage 100cloud. Dashboards can be connected through Business Intelligence, financials through Sage 100cloud Intelligence, and exception monitoring and alerting through sage 100c Alerts & Workflow, to name a few. The emphasis with Sage 100cloud is to give you more information so you can make better decisions and be that trusted name for your customers.

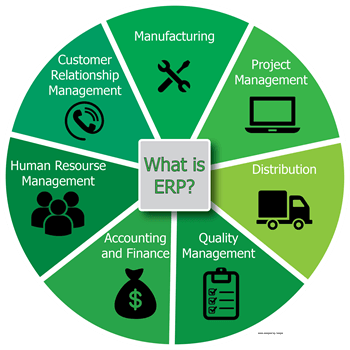

What is ERP solution?

ERP solution software unifies the systems your organization uses every day – everything from product development and supply chain management, to distribution management and more. ERP solution software utilizes a suite of business applications designed to improve business management and help you focus on core business. Organizations use ERP solution software to manage and organize the data that makes their business run. When you bring on the right ERP solution system, you will have access to better collaboration, reporting data, productivity, and maximized production.

ERP solution technology offers substantial benefits. Contact Yeo & Yeo Technology to learn more about Sage 100cloud erp solution software.

A slew of different construction-focused accounting systems are available, but not all of them may be a good option for your company. For the small- and medium-size company, some of the dedicated systems can be too robust or too pricey to be a viable option. For this reason, many companies have turned to QuickBooks for their accounting needs. Construction owners and managers can successfully utilize this platform with the help of various add-on applications.

Intuit’s website describes the many different Intuit-approved applications that will integrate seamlessly with the various QuickBooks platforms. These add-ons give users functionality that is not built into the basic QuickBooks system. Below are a few examples of popular construction-related add-ons and what they can do for users.

- Corecon

Corecon is an overall project management software. With Corecon, contractors can easily monitor their job costs, build accurate estimates and bids, and schedule jobs. Corecon also gives staff working on job sites the ability to enter their logs and timecards through a mobile app.

- RedTeam

RedTeam assists contractors with the internal management of jobs. With this app, contractors can do paperless posting and approval of vendor and subcontractor invoices, easily track subcontractor insurance and other credentials, and track revenue based on each job’s percentage of completion.

- Knowify for Contractors

Knowify is made specifically for residential contractors. It gives these companies the ability to build bids for both general contractor jobs as well as smaller jobs with property owners. It helps contractors estimate jobs and track job costs once it has begun, support both standard and AIA-style invoicing, maintain online schedules, and create and automatically send purchase orders to vendors.

The above are just a few examples of the different add-ons that are available; many more are offered that can help construction contractors manage documents, generate advanced reporting, simplify payroll and optimize productivity.

Call on the members of Yeo & Yeo’s Computer Accounting Software Solutions Team who hold QuickBooks accreditations and can help you choose software that will provide the most substantial benefits for your construction business.

Auto-enrolling 401(k) plan participants without also incorporating an auto-escalation feature might be a counterproductive exercise. J.P. Morgan Asset Management survey data suggests that average 401(k) plan deferral rates have been trending downward even though more employers are adopting auto-enrollment. The apparent culprit: low auto-deferral rates.

Stats tell the story

From 2012 to 2014, the average annual contribution rate was 7.2%. This is down slightly from the 7.4% average in the prior two-year period, and well below the 8% average during 2007 to 2008.

Even though 45% of surveyed employers auto-enroll new participants, just 31% have auto-escalation features built in. One interesting note from the study: For plans with at least $200 million in assets, the numbers are considerably higher — 62% of these high-asset plans have automatic enrollment and 48% use auto-escalation clauses.

The most common auto-enrollment default deferral rate is only 3%, according to the most recent Defined Contribution Institutional Investment Association (DCIIA) survey. Participants who defaulted into such a low deferral rate generally do not increase it significantly. With typical annual auto-increase increments of only 1%, it will take new employees several years to begin deferring at reasonable levels, and many more to reach the 15% that DCIIA sees as ideal.

The DCIIA survey reveals impressive deferral rates for plans that both auto-enroll and auto-escalate participants. “Plan sponsors who offer both automatic enrollment and automatic contribution escalation have over twice as many participants with retirement savings rates over 15% (14% of respondents) as those that do not offer both (6% of respondents),” according to the survey.

Change is in the air

So why don’t plan sponsors implement these features? According to the survey, plan sponsors with less than $50 million in plan assets were concerned about complaints from participants (28%) and feared it would be seen as paternalistic (18%). And a whopping 31% have never considered using it.

But the DCIIA study concluded that, when properly implemented, automatic features can make a positive difference. Contact your benefits specialist to learn how to use both auto-enrollment and auto-escalation clauses to help benefit your employees.

© 2016

Manufacturers across the country have become a main target for cybercriminals. The news, trade journals, and professional organizations such as the Michigan Manufacturers Association all have stressed the importance of manufacturers becoming aware of this growing threat.

- IBM released a study in 2016 titled, X-Force Research 2016 cybersecurity Intelligence Index, which found that the manufacturing sector was second only to healthcare as the most attacked industry in the country.

- The most recent Carbon Black Threat Report places the manufacturing industry at the top of the target lists for ransomware and malware.

- According to the Ponemom Institute, the average price for a small business to clean up after they have been hacked stands at $690,000; for mid-market companies, it is more than $1 million.

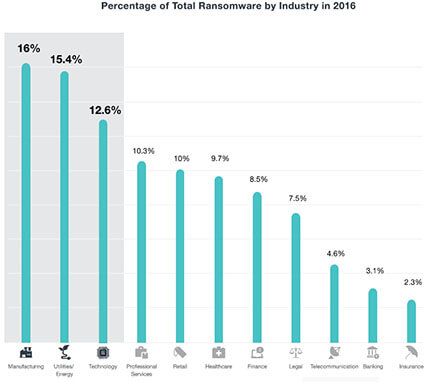

The Carbon Black Threat Report states that when considering the total amount of ransomware seen in 2016, manufacturing companies (16% of total ransomware instances), utility/energy companies (15.4% of all ransomware instances) and technology companies (12.6% of all ransomware instances) led the way.

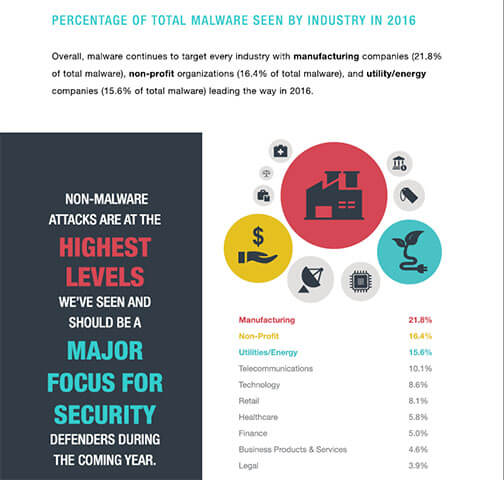

The Carbon Black Threat Report also states that overall, malware continues to target every industry with manufacturing companies (21.8% of total malware), non-profit organizations (16.4% of total malware), and utility/energy companies (15.6% of total malware) leading the way in 2016.

Percentage of Total Malware Seen by Industry in 2016

What should manufacturers do?

What can manufacturers do to protect their organizations? It starts with understanding the threats and risks that exist and how to defend against them. Cybersecurity protection has become a requirement for manufacturers who do business with several agencies and they must be compliant as soon as December 2017. If you are unsure of your organization’s cybersecurity needs or risks, it is important to partner with a technology firm that has expertise in this area.

Next Generation firewall, anti-virus and spam protection services – together with proactively monitoring and managing your network hardware, software, and data traffic – can effectively reduce the risk of a disastrous attack. But firewalls and the best security systems in the world cannot stop everything. Manufacturers should also consider implementing a security awareness training program, which has proven to improve many security flaws. By making employees the first line of defense, manufacturers have a cost-effective way to strengthen the security of their organization.

Call on the members of Yeo & Yeo’s Manufacturing Services Group, who can help you understand and protect your business with industry best practices and technology solutions.

There is a common scene in popular literature, television shows and movies. The family of a wealthy individual gathers in an attorney’s well-appointed office to hear the reading of a recently deceased’s will. Each member usually represents a given stereotype — the spendthrift, the frugal one, the outsider — and, together, they wait impatiently for the attorney to reveal what they are getting.

In real life, this is not how an estate plan should work. To keep the mystery to a minimum, it is a good idea to hold occasional, if not regular, family meetings about your estate plan. Let’s look at some key points to consider when setting up these critical and informative gatherings.

Guest list

Whom should you invite? Start with your spouse, children and other family members who will be affected by your plan (either by their inclusion or exclusion). You should also invite any nonfamily members you will ask to serve as executors, trustees, agents, or guardians of minor children.

Also, request the presence of key advisors such as your attorney and accountant. They can be of service for two important reasons:

1. Questions and answers. Advisors can help answer questions about how your plan works. The legal machinations of an estate plan are complex, and the tax laws involved are not simple either. Your family will better understand the details of your plan if an expert explains them.

2. Team building. The meetings create an opportunity for your family, representatives and advisors to get to know one another. Getting acquainted now will help them build trust and, thereby, improve the chances that your plan will operate smoothly when the time comes for it to do so.

Agenda items

The meetings will need to include a number of agenda items. For starters, you should review the key documents that make up your plan and let everyone know where they are located. In addition, provide an overview of the estate planning decisions you have made so far and — most important — the reasoning behind them.

Many people simply divide their assets equally among their heirs. But in estate planning, equal is not necessarily fair. For example, let’s suppose Tara has adult children from a previous marriage and younger children from her current marriage. She put her older children through college years ago, and now they are gainfully employed and financially independent.

Fairness would dictate that Tara’s estate plan favor her younger children, who will need the money for tuition and living expenses. But her older children may not see it that way unless she explains it to them. A family meeting provides an opportunity for that discussion.

Other issues to discuss include charitable giving, the treatment of assets with special significance — such as vacation homes or family heirlooms — and decisions about which family members are chosen to be guardians, executors and so on.

Business matters

Family meetings are particularly valuable when a family business is involved. It may seem fair to provide a greater share to family members who work in the business.

But what if most of your wealth is tied up in the business? How do you provide for those who do not work in the business while still rewarding the “sweat equity” of those who do?

One option is to divide ownership equally but to use voting and nonvoting stock to give management control to family members who work in the business. Another option is to leave the business to those who work in it and use life insurance to create an inheritance for those who do not. Whatever the solution, the best way to avoid conflict and resentment is to discuss the issue with all interested parties and get their input.

Comforting experience

The thought of sitting down with family members and discussing what eventually is to become of your estate may seem awkward. But, often, the most uncomfortable meeting is the very first one. Once the topic is broached and the details are being discussed, many families find the experience comforting and informative. Again, involve your advisors in the planning and carrying out of the meetings and the process is likely to go much more smoothly.

© 2015

Because of a weekend and a Washington, D.C., holiday, the 2016 tax return filing deadline for individual taxpayers is Tuesday, April 18. The IRS considers a paper return that’s due April 18 to be timely filed if it’s postmarked by midnight. But dropping your return in a mailbox on the 18th may not be sufficient.

An example

Let’s say you mail your return with a payment on April 18, but the envelope gets lost. You don’t figure this out until a couple of months later when you notice that the check still hasn’t cleared.

You then refile and send a new check. Despite your efforts to timely file and pay, you’re hit with failure-to-file and failure-to-pay penalties totaling $1,500.

Avoiding penalty risk

To avoid this risk, use certified or registered mail or one of the private delivery services designated by the IRS to comply with the timely filing rule, such as:

- DHL Express 9:00, Express 10:30, Express 12:00 or Express Envelope,

- FedEx First Overnight, Priority Overnight, Standard Overnight or 2Day, or

- UPS Next Day Air Early A.M., Next Day Air, Next Day Air Saver, 2nd Day Air A.M. or 2nd Day Air.

Beware: If you use an unauthorized delivery service, your return isn’t “filed” until the IRS receives it. See IRS.gov for a complete list of authorized services.

Another option

If you’re concerned about meeting the April 18 deadline, another option is to file for an extension. If you owe tax, you’ll still need to pay that by April 18 to avoid risk of late-payment penalties as well as interest.

If you’re owed a refund and file late, you won’t be charged a failure-to-file penalty. However, filing for an extension may still be a good idea.

We can help you determine if filing for an extension makes sense for you — and help estimate whether you owe tax and how much you should pay by April 18.

© 2017

Audits don’t have to be stressful with proper preparation.

Yeo & Yeo has streamlined its approach to audits. We have implemented procedures to complete the audit efficiently using state-of-the-art technology and our knowledge of ever-changing audit and accounting standards. Our approach balances compliance with providing superior services at competitive pricing.

Download my presentation, Preparing for a Headache-free Audit, to become familiar with the audit process and learn tips and trick for preparation.

If your organization receives federal funds, whether from a pass-through entity, such as the State of Michigan, or directly from the federal government, you need to be aware that the Uniform Grant Guidance 2 CFR 200 is now applicable. I encourage you to stay informed and not to fear because UGG can be more streamlined than you originally believed.

Download my presentation, Don’t Say UGH! to UGG Procurement, for a brief summary of the changes.

Kati Krueger of Yeo & Yeo’s Medical Billing affiliate, a provider of practice management consulting and medical billing services, attended the Medical Billing Executive Conference held March 13-15, 2017, in New Orleans.

The three-day conference provided medical billing executives with an in-depth understanding of important industry developments including:

- New Medicare quality payment program and 2017 billing updates

- How to maximize medical practice revenue

- Physician revenue cycle management 2020 – a three-year outlook

- Performance benchmarks for physician practices

“The conference provided benchmarks for medical billing service providers and their clients, updates, and insight as to what services we may offer our clients in the future. Attending conferences of this caliber increases our depth of knowledge and is critical for us to proactively advise our clients,” says Krueger, vice president of Yeo & Yeo’s Medical Billing affiliate.

More than 50 medical billing executives from throughout the country attended training sessions to help them manage their medical billing companies more effectively, discuss critical issues and share best practices and solutions.